Have you ever looked at your monthly expenses and wondered where all your money really goes?

Rent to your landlord. Car payment to the bank. Groceries to massive food corporations. Netflix, Spotify, Amazon Prime — all flowing to shareholders you’ll never meet.

Every single day, your hard-earned money travels from your pocket directly into the accounts of capital owners. They collect while you work. They profit while you pay.

The Invisible Transfer System

I used to think this was just how life worked.

You work, you pay bills, you try to save what’s left. Maybe invest some spare change if you’re lucky. Repeat until retirement, hoping the math somehow works out.

Then I started adding up the numbers.

My monthly “invoice” to capital owners was staggering. Rent: $2,400 to a property management company. Car payment: $450 to a bank. Insurance: $200 to shareholders of a massive corporation. Utilities: $300 to energy companies. Subscriptions: $150 to various tech platforms.

That’s $3,500 every single month flowing away from me — before I even bought food or coffee.

Multiply that by 12 months. Then by 10 years. I was looking at hundreds of thousands of dollars transferred from my bank account to people who already had plenty.

The realization hit me like a brick: I wasn’t just paying bills. I was funding other people’s wealth.

Why Your Paycheck Goes to Everyone Else First

Here’s what nobody tells you about money flow.

When you receive your paycheck, you immediately become a distribution system. Your salary gets parceled out to dozens of capital owners who provide the things you need to live.

You rent their apartments. Drive their cars. Use their electricity. Stream their content. Shop at their stores.

They designed it this way.

Capital owners create systems that capture recurring payments from millions of people like you. They build the infrastructure you depend on, then charge you monthly fees to access it.

Your job is to work hard enough to afford these payments. Their job is to collect them.

The fundamental question becomes: Which side of this equation do you want to be on?

The Golf Ball Revolution

Warren Buffett figured this out when he was twelve years old.

Young Warren would scour golf courses, collecting lost balls from water hazards and rough patches. He’d clean them up and sell 12 balls for $6. Not bad for a kid.

But here’s the genius part: Warren didn’t keep doing this forever.

He took that $6 and bought something that would generate money without him having to wade through swamp water every day. A small piece of a business. Then another. Then another.

Eventually, those assets started sending him money while he slept.

The shift from “selling his time” to “owning things that pay him” changed everything. Instead of being the one who pays, he became the one who gets paid.

This is the pivot every wealth-builder makes: Stop trading time for money. Start buying assets that generate money.

What Capital Owners Know (That You Don’t)

Rich people ask a different question than the rest of us.

When they get money, they don’t ask: “What should I do to earn more?”

They ask: “What should I buy that will pay me?”

This single shift in thinking explains why some people escape the paycheck-to-bills cycle while others stay trapped for decades.

Think about it. A rental property owner asks: “What building should I buy?” A stock investor asks: “What company shares should I buy?” A business owner asks: “What system should I buy or build?”

Meanwhile, most people ask: “What job should I get? What skill should I learn? What certification should I pursue?”

Both paths require effort. But only one path leads to money flowing toward you instead of away from you.

The wealthy understand that capital is stored demand. When you own something people need — shelter, transportation, food, entertainment, technology — you capture a piece of that demand.

Every month, that demand translates into cash flow directed to you.

How to Stop Making Rich People Richer

The solution isn’t complicated, but it requires discipline.

Pay yourself first. Before the landlord, before the car payment, before Netflix.

This sounds impossible when you’re already stretched thin. But here’s what actually happens when you flip the order.

Instead of investing your leftovers, you invest first and then figure out how to cover your bills with what remains. This creates productive pressure.

You might pick up a side project. You might negotiate a raise. You might cancel subscriptions you barely use. You might find a cheaper apartment.

The key insight: When you invest first, you become resourceful about everything else.

Start small. Even $100 a month flowing toward asset ownership instead of pure consumption changes the trajectory.

Buy index funds that give you ownership stakes in hundreds of companies. Those companies’ employees work to generate profits, and you receive a portion as a shareholder.

Buy dividend-paying stocks that send you checks quarterly. Buy REITs that collect rent from tenants and distribute it to you.

The amounts seem tiny at first. But remember: you’re reversing a fundamental flow. Instead of money leaving your account permanently, money starts arriving in your account regularly.

The Compound Effect of Keeping Your Money

Here’s what happens when you consistently redirect money flow toward asset ownership.

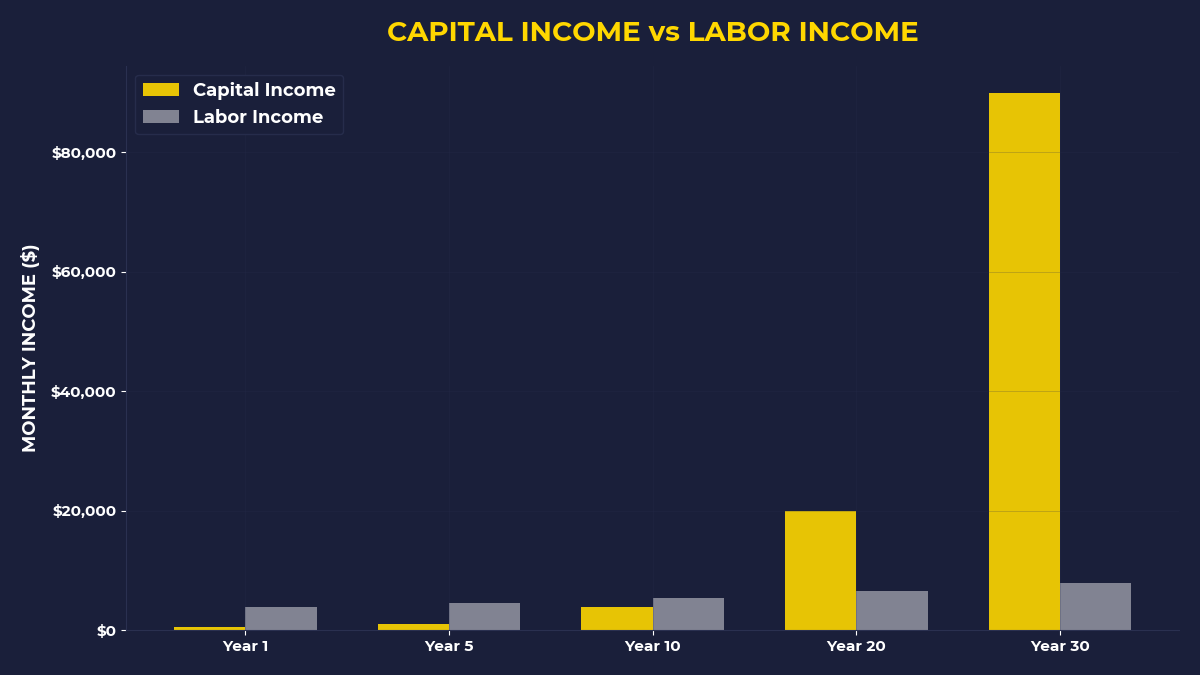

Year one: Your assets might generate $200 in cash flow. Barely noticeable.

Year three: $800 in annual cash flow. Now you’re covering a monthly bill.

Year five: $2,000 in annual cash flow. That’s rent money.

Year ten: $8,000+ in annual cash flow. Multiple bills covered by assets, not job income.

The math accelerates because you’re not just saving money — you’re redirecting cash flow from consumption to ownership.

Those assets compound. Dividends get reinvested. Share prices appreciate. Rental properties increase in value and rent.

Meanwhile, every dollar you would have spent on unnecessary consumption was instead transformed into an income-generating machine.

This is how people escape the cycle of working harder to afford higher bills.

The One Thing To Remember

Every dollar you spend makes someone else richer — unless you spend it on assets that make you richer. The wealthy didn’t get wealthy by working for money; they got wealthy by making money work for them. Your escape from the bills-and-paycheck treadmill begins the moment you start asking “What should I buy?” instead of “What should I do?”

Track where your money goes for one month — you’ll be shocked how much flows to capital owners

Set up automatic investing of at least 10% of your income before paying any discretionary bills

Start with broad market index funds or dividend ETFs — simple ownership stakes in profitable businesses

🎬 Prefer watching? Check out the video version on YouTube: