The Safety First Trap

Sarah — 29, marketing coordinator in Denver — opened her investment app for the third time that morning. Her finger hovered over the “Buy” button for an S&P 500 ETF, then pulled back. Again. She’d been doing this dance for six months, paralyzed by the same question: “What if I lose it all?”

Her savings account held $23,000. Safe. Guaranteed. Earning 0.5% annually while inflation chewed through her purchasing power like termites through wood.

Sarah’s investment philosophy, like most people’s, wasn’t built on logic. It was built on terror.

I Used To Be Sarah

I get it because I lived it. At 27, I had $31,000 sitting in a high-yield savings account earning 1.2% — I thought I was being smart. My investment philosophy back then was simple: don’t lose money. Period.

The problem with that philosophy? It’s actually a guarantee that you will lose money. Just slowly. Invisibly. Every single day.

Here’s what I wish someone had told me then: your money anxiety isn’t protecting you from risk. It’s creating the biggest risk of all — staying poor forever.

I remember the exact moment this clicked for me. I was sitting in my Honda Civic outside a Starbucks, calculating how much rent money I was sending to my landlord every month. $1,850. Times 12 months. $22,200 annually. Going to someone who owned something I needed every day.

That’s when I realized my investment philosophy was backwards. I wasn’t trying to build wealth. I was trying to avoid feeling stupid.

Capital Stores Demand, Not Money

Most people think capital is money in a bank account. It’s not. Capital is stored demand — owning pieces of things people need, want, and pay for repeatedly.

Sarah’s $23,000 in savings? That’s not capital. That’s cash waiting to become someone else’s capital the moment she spends it on rent, groceries, or her Netflix subscription.

Every month, Sarah sends money to capital owners:

• $1,200 to her landlord (who owns real estate)

• $400 to her car payment (bank owns the loan)

• $150 to various subscription services (companies own the platforms)

• $800 on groceries and daily expenses (retailers and brands own the distribution)

That’s $2,550 monthly — $30,600 annually — flowing from Sarah to people who own things she needs.

Her investment philosophy focused on not losing money. But she was already losing $30,600 every year by design.

The Warren Buffett Golf Ball Lesson

When Warren Buffett was a kid, he picked up lost golf balls around courses and sold them for 6 cents each. Hard work. Direct trade of time for money.

But here’s the part most people miss: Buffett took that money and bought assets. Not more golf balls to pick up himself. Assets that other people would work to make profitable.

The golf ball picking was temporary. The asset buying was permanent.

Your investment philosophy should answer one question: “What should I buy?” Not “What should I do?” Not “How can I avoid losing money?” Not “What if the market crashes?”

What should I buy that people will pay for, whether I’m working or sleeping?

Why Your Brain Sabotages This Simple Logic

Your brain evolved to keep you alive in a world where losing resources meant death. Modern markets punish this ancient wiring.

When Sarah looks at that “Buy” button, her amygdala screams warnings about loss. But it can’t calculate the compound cost of inaction over 30 years.

Fear feels immediate. Opportunity cost feels abstract.

This is why 78% of people never build significant wealth despite earning decent incomes. Their investment philosophy optimizes for feeling safe today instead of being rich tomorrow.

I learned this the expensive way. By age 30, I’d “safely” kept $40,000 in savings accounts for four years. If I’d bought index funds instead, that money would have grown to around $65,000 by the time I finally started investing.

My fear-based investment philosophy cost me $25,000 in opportunity. Plus all the compound growth on that $25,000 forever.

Are You Building Wealth Or Building Comfort?

Here’s the reframe that changed everything for me: there are only two types of people in the economy. People who own demand, and people who pay for it.

Sarah pays rent because her landlord owns real estate demand. She pays her car loan because the bank owns credit demand. She pays for Netflix because they own entertainment demand.

Every dollar she “safely” keeps in savings is a dollar that’s not buying her a piece of the demand she pays for every day.

The question isn’t whether investing is risky. The question is whether staying poor is riskier than trying to get rich.

For Sarah, keeping $23,000 in savings feels safe. But she’ll send $306,000 to landlords over the next 10 years if rent increases at 3% annually. Her “safe” money will grow to maybe $25,000 over the same period.

Which scenario is actually riskier?

The Demand-First Investment Philosophy

My investment philosophy now starts with a simple question: what do people pay for every single day, whether they want to or not?

Food. Shelter. Transportation. Communication. Entertainment. Healthcare. Energy.

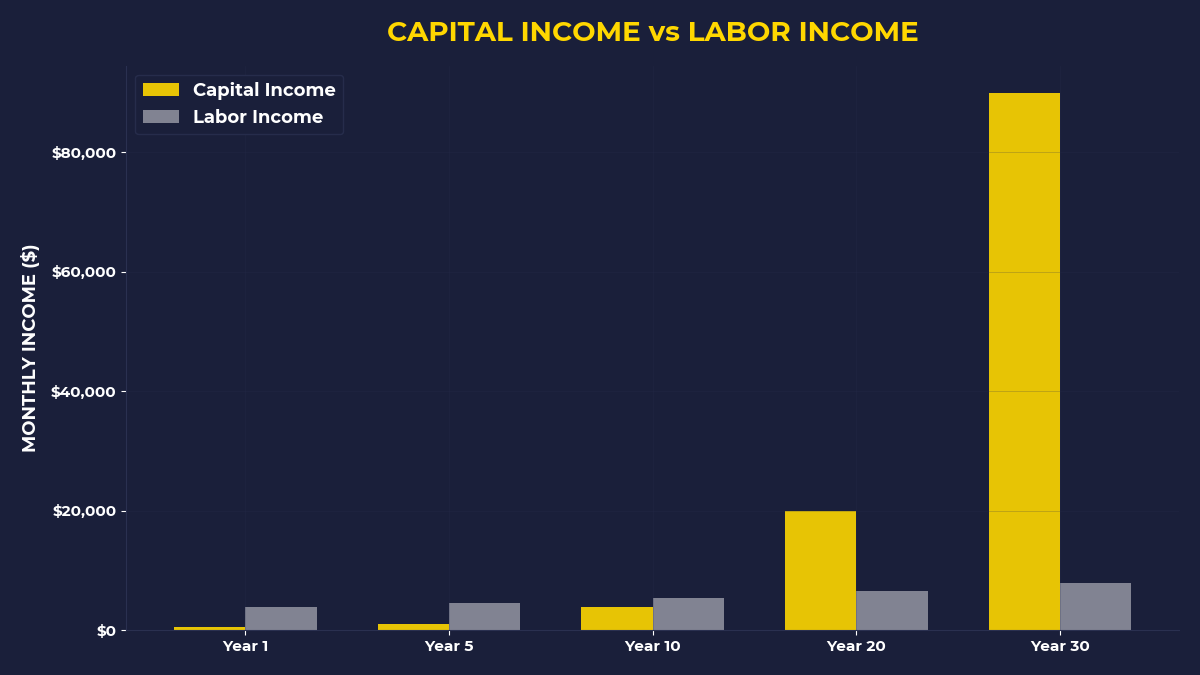

Instead of trying to time markets or pick winners, I buy pieces of the companies that own demand in these categories. When Sarah pays her electric bill, a tiny fraction flows to me through utility stocks. When she buys groceries, consumer staple companies I own get a cut.

I’m not predicting what will happen to the market next month. I’m betting that people will keep needing electricity and food next decade.

This isn’t about being smart. It’s about switching sides — from always paying for demand to sometimes owning it.

The One Thing To Remember

Your current investment philosophy probably isn’t serving you. If it was, you’d already have enough capital to stop working. The difference between staying poor and building wealth isn’t intelligence or luck — it’s asking “What should I buy?” instead of “What if I lose money?” Every month you wait is another month sending your paycheck to people who figured this out before you did.

• Before you pay any bill this month, transfer $200 into a brokerage account and buy index funds

• Calculate how much you send to capital owners monthly (rent, car payment, subscriptions) — that number should motivate you

• Replace “What if I lose money?” with “What if I never own anything?” in your internal dialogue

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.