The hardest workers I have ever met are not rich. Most of them never will be. Not because they lack discipline, or intelligence, or drive — but because every ounce of their energy is directed at the wrong question.

They keep asking: what should I do?

The question they never ask — the one that actually separates people who accumulate capital from people who just accumulate fatigue — is this: what should I buy?

The Thing I Got Wrong for the Better Part of My Twenties

I used to believe that effort was the variable. Work harder, earn more, save more, repeat. I tracked every hour. I optimized my morning routine. I read the productivity books. I was, by almost any external measure, doing the things you’re supposed to do.

Then I watched a friend — less disciplined than me, worse at his job than I was at mine — quietly accumulate a position in a handful of dividend-paying businesses over about six years. By 2019, that portfolio was generating roughly $2,200 a month without him doing anything. Meanwhile, I was still converting hours into dollars at a fixed rate and calling it a career.

That was the crack in the foundation. I hadn’t been building capital. I had been renting myself out — to employers, to clients, to the market for skilled labor — and calling it wealth-building. It wasn’t. It was sophisticated subsistence.

Here’s the thing. Effort is necessary but not sufficient. Effort without ownership is just expensive labor.

Capital Is Not What Your Bank Statement Says It Is

Most people think capital is money. Accumulated dollars. A number in an account. This is the first wrong turn, and almost everything that follows from it is also wrong.

Capital is stored demand. That’s the reframe that changes everything.

Think about why a famous musician earns millions while a technically superior musician earns nothing. It isn’t talent. There are thousands of musicians with more technical skill than the ones selling out arenas. The difference is demand. Concentrated, durable, recurring demand. And when you own something that sits at the center of that demand — a catalog, a brand, a platform, a stake in a company with a durable moat — you own a structure that collects that demand on your behalf, whether you show up or not.

That’s what capital does. It harvests demand automatically. Your labor, by contrast, only harvests demand when you are physically present to perform it. The moment you stop showing up, the cash flow stops. Capital keeps going.

Every bill you pay every month is proof of this. Your rent check, your mortgage, your electricity, your grocery tab, your streaming subscriptions, your car payment — each one of those is a demand transfer. Someone who owns a stake in the structure that sits between you and what you need collects a piece of your income every single month, automatically, while they sleep. You are the recurring revenue in someone else’s compound interest machine.

Wild, right? Not metaphorically. Literally. Your monthly routine is their business model.

Why Smart People Stay on the Wrong Side of This

What drives intelligent people to keep optimizing their output instead of buying demand? Mostly it’s the herd instinct — one of the oldest and most destructive forces in personal finance.

From childhood, the message is uniform: get good grades, develop marketable skills, find a stable job, work hard, get promoted. Every person around you reinforces this. Your parents lived it. Your school taught it. Your employer profits from it. The entire cultural narrative around “success” is built on the premise that what you do is what determines what you have.

The herd runs in one direction. It feels dangerous — almost disloyal — to step off that path and ask whether the path itself is the problem.

But look at the math. The median American worker earned about $59,400 in 2023. After taxes, insurance, and basic living expenses, the average household saves roughly 4.5% of disposable income — around $2,200 per year. At that savings rate, converting labor into wealth is not a strategy. It is a treadmill with a slight incline.

The problem isn’t the worker. The problem is the framework.

What Compound Interest Actually Means (It’s Not What the Textbooks Say)

There’s a story about Warren Buffett as a child that I keep coming back to. Around age 11, he started collecting lost golf balls near a course in Omaha and reselling them — a dozen for $6. He was converting his labor into a small but real cash flow. Fine. Most kids stop there.

But Buffett didn’t. He rolled those early earnings into a used pinball machine, then a small stake in a farmland rental, then into stocks. Each asset generated cash flow. Each cash flow bought more assets. The thing he was building — long before he could articulate the theory — was a compounding structure where demand-generating assets funded the acquisition of more demand-generating assets.

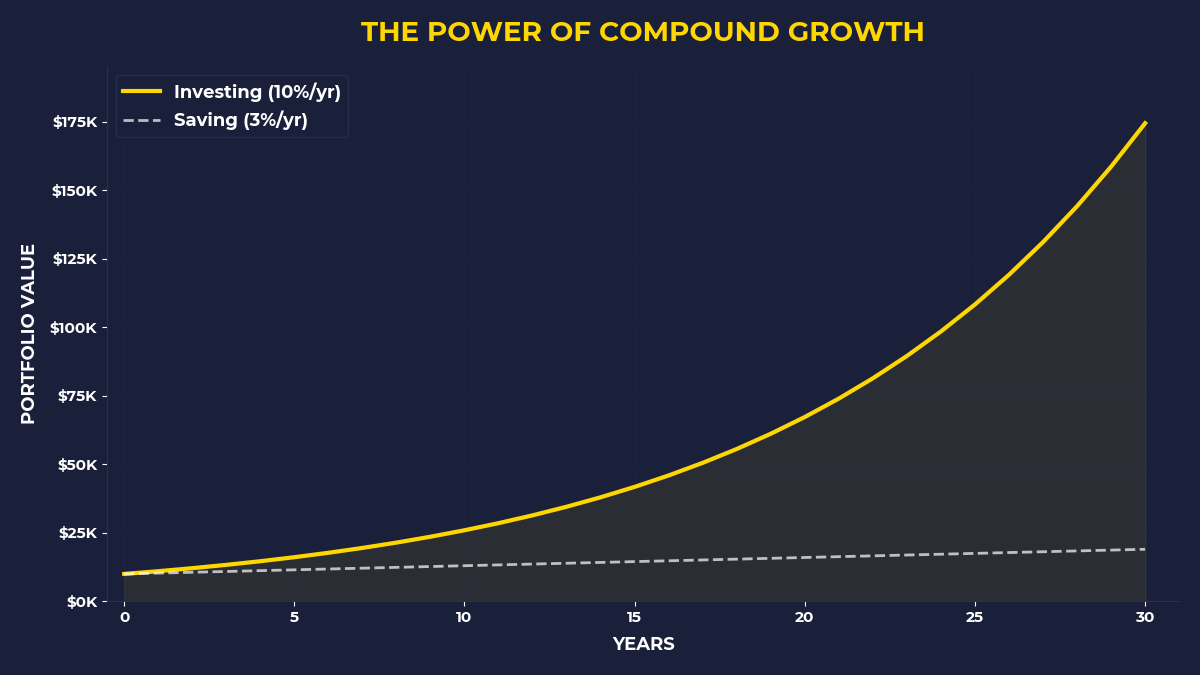

That’s what compound interest actually is. Not a savings account growing at 4.5% annually. Not a bond ladder. It’s the recursive loop of buying something that attracts demand, harvesting the cash that demand produces, and immediately deploying that cash to buy more demand.

There’s a related story from a book Buffett read as a teenager — a story about a man named Harry who noticed a coin-operated scale in a pharmacy and watched eight strangers use it in twenty minutes. He bought three scales for $175, generated $98 per month in passive income, and then — here’s the part that stuck — he used the income from those three scales to buy 67 more. By the end, he owned 70 machines. The last 67 were purchased entirely with the cash flows from the first three.

That’s not luck. That’s a structure. One that most people never build because they’re too busy answering the question of what to do next.

What Does It Actually Mean to Buy Demand?

What assets actually hold demand? Let me be honest — this is where the concept needs to land in your portfolio, not just your philosophy.

A business with a durable competitive advantage holds demand. An index fund tracking the S&P 500 — which returned approximately 10.7% annually between 1993 and 2023, including dividends — is a fractional stake in thousands of businesses that collectively harvest enormous amounts of human demand every single day. A rental property in a supply-constrained city holds demand. A content platform, a patent portfolio, a brand — these are structures that demand flows through, and owning a piece of the structure means demand flows to you.

What does not hold demand? Your salary. Your bank balance. Your emergency fund sitting in a 0.5% savings account while inflation runs at 3.4%. Cash is not stored demand. Cash is stored optionality that decays. The only way to preserve it is to deploy it into something that sits inside a demand current.

This is why the first question of the serious investor is never “how do I grow my savings?” It’s “what should I buy, and does it sit in the path of durable human demand?”

The Leverage Problem Nobody Talks About Honestly

Once you understand that capital is stored demand, and that buying demand-bearing assets is the mechanism, a third idea becomes obvious: you need leverage to accelerate the loop.

Not leverage in the reckless, margin-call sense. Structural leverage. The kind that means your assets are doing work you’re not doing yourself.

Back to the young Buffett for a second. When he was collecting golf balls alone, his output was capped by his own physical capacity. The moment he could hypothetically employ two friends — one to retrieve balls, one to clean them — and pay each $2 per dozen while collecting $6 per dozen himself, his earnings per hour jumped dramatically without any increase in his own labor. The system worked without him at the center of it. That’s leverage.

For most people reading this, the practical version is simpler than building a business empire. It’s owning equity in companies whose employees show up every day and whose systems serve customers you’ll never meet. Every share of a quality business is a tiny piece of leverage — someone else’s effort and creativity working on your behalf, generating demand, producing cash flow, compounding quietly in the background.

The S&P 500 dropped 57% between October 2007 and March 2009. The people who understood structural leverage — who knew they owned a piece of durable human demand, not a number on a screen — bought more. The people who understood only the price watched in horror and sold at the bottom. Fear, the oldest and most expensive primate instinct, made the decision for them.

If You’ve Been Doing Everything Right and Still Feel Behind, This Is Why

Are you the person who has done the responsible things — contributed to your 401(k), built an emergency fund, maybe even picked a few stocks — but still feels like the engine isn’t running at full power?

Here’s what’s probably happening. You have been treating capital accumulation as a savings problem when it’s actually an ownership problem. Savings is the raw material. Ownership is the structure that transforms the raw material into something that compounds.

You need both. But savings without ownership is just a pile of rocks. Ownership is the quarry that turns the rock pile into a building that generates rent.

A friend of mine — software engineer, excellent salary, genuinely smart — told me three years ago that he kept about $80,000 in a high-yield savings account “waiting for the right moment to invest.” That $80,000, deployed into a broad equity index in early 2020 during the pandemic crash, would have been worth approximately $158,000 by the end of 2023. Instead, it earned roughly $12,000 in interest over four years — and lost purchasing power in real terms against 2021-2022 inflation. The instinct that kept him in cash felt like prudence. It was actually recency bias dressed up as caution.

The right moment was the moment it felt most wrong. It always is.

What the Primal Investor Takes Away

Redefine capital immediately. Capital is not money in an account. It is a structural position inside a flow of durable human demand. Every investment decision starts by asking whether the asset sits inside such a flow — not whether it “seems safe.”

Change the primary question. Before evaluating any financial decision — career move, side project, investment — ask “what should I buy here?” not “what should I do?” The buying question forces you to think in ownership and cash flows. The doing question keeps you in the labor mindset.

Build the recursive loop, even small. If you invest 15% of your income and reinvest every dividend and distribution back into more equity, you have a compound structure. If you spend every dollar you make and invest nothing, you have a job. Even $400 per month into a low-cost broad equity index, started at age 30 and held for 30 years at historical average returns, produces approximately $900,000. The structure matters more than the amount.

Recognize the herd instinct before it fires. When the market feels catastrophically dangerous — when every headline confirms that things are falling apart — the primate brain reads this as a signal to flee the herd. That instinct evolved to keep you alive on the savanna. In financial markets, it transfers your demand-bearing assets to the person willing to hold them. Name the instinct in the moment. Then act against it.

Leverage is not a dirty word — it’s the mechanism. Owning equity in companies where other people’s effort compounds on your behalf is the cleanest form of leverage available to any investor. Use it. Buy a watermelon slice, not a single strawberry.

The question was never how hard you work. The question was always what you own while you’re working.

Stop building someone else’s demand machine. Go buy a piece of your own.

🎬 Prefer watching? Check out the video version on YouTube:

")