Marcus called me at 11:47 PM on a Tuesday. Age 28, marketing manager at a mid-sized firm in Denver, making $67,000 a year. His voice was shaky.

“I just got off a Reddit thread about contrarian investing,” he said. “Everyone’s talking about buying the dip, waiting for crashes, being greedy when others are fearful. But I can’t even afford to be greedy when I’m fearful. My checking account has $340 in it, and rent’s due in five days.”

Marcus had read every contrarian investing book. He understood the theory. Buy low, sell high. Zig when others zag. Be patient when others panic. But all that wisdom felt useless when his biggest financial crisis wasn’t market volatility—it was making it to his next paycheck without overdrafting.

“How can I be contrarian,” he asked, “when I don’t even have money to invest?”

I Used To Think the Same Thing

I know exactly how Marcus felt because I was there too. Seven years ago, I was 29 and making $52,000 as a content writer. I’d read about Warren Buffett buying Coca-Cola during market downturns, about value investors scooping up bargains while everyone else panicked.

Here’s the thing. I thought contrarian investing meant having cash reserves to deploy when assets got cheap.

I was wrong. Dead wrong.

The real contrarian move isn’t buying when markets crash. Most people can’t time that anyway. The real contrarian move is buying before you pay your bills. Buying when you’re broke. Buying when it feels impossible.

I learned this the hard way one March morning when my rent was due, my account had $890, and my rent was $850. I had $40 left for food, gas, everything else. That morning, I did something that felt insane: I bought $200 worth of stock. Then I figured out how to make rent work.

That decision changed my relationship with money forever.

What Nobody Tells You About Capital

Every month, Marcus was playing the same game 73% of Americans play. Paycheck arrives. Bills get paid. Groceries, gas, subscriptions, debt payments. Whatever’s left over—if anything—goes into savings.

This feels responsible. It feels adult. It feels like what financially smart people do.

It’s actually the exact opposite of how capital gets built.

Think about Warren Buffett’s childhood story—the one where he collected lost golf balls from the local course and sold them for $6 per dozen. He could have spent that money on candy, toys, comic books. Normal kid stuff.

Instead, he did something contrarian: he bought a pinball machine for $25 and placed it in a barbershop. The machine generated quarters while he slept, studied, played with friends. That cash flow bought him a second pinball machine. Then a third.

The contrarian insight wasn’t timing—it was priority. Pay yourself first, figure out survival second.

Why Your Bills Are Invoices From Capital Owners

Look at your bank statement from last month. Really look.

Your rent payment went to someone who owns real estate. Your car payment went to someone who owns financing capital. Your Netflix subscription went to shareholders. Your grocery bill went to supply chain owners, brand owners, retail owners.

Even your morning coffee—$4.75 to Starbucks—went to capital owners.

You sent cash to capital owners approximately 47 times last month. How many times did capital owners send cash to you?

If the answer is zero, you’re on the wrong side of capitalism.

The contrarian realization: every dollar you spend before buying assets is a dollar that could have been working for you instead of against you.

The $50 Experiment That Breaks Everything

Here’s what I told Marcus, and here’s what I’m telling you: before you pay a single bill this month, move $50 into a brokerage account and buy stock. Any stock. I don’t care if it’s Apple, Google, or a boring index fund.

“But what if I can’t make rent?” he asked.

Figure it out. Work an extra shift. Sell something. Ask for an advance. Skip restaurants for two weeks. The point isn’t the $50—it’s breaking the mental pattern that bills come first.

Because here’s what happens when you flip that script: suddenly you’re thinking like a capital owner instead of a capital renter.

When your first priority is buying assets, your brain starts solving different problems. Instead of “How do I stretch this paycheck?” you start asking “How do I generate more cash to buy more assets?”

That shift in questioning changes everything.

The Real Contrarian Truth About Market Timing

Most people think contrarian investing means being smart about when to buy. Wait for crashes. Buy when others are selling. Time the market perfectly.

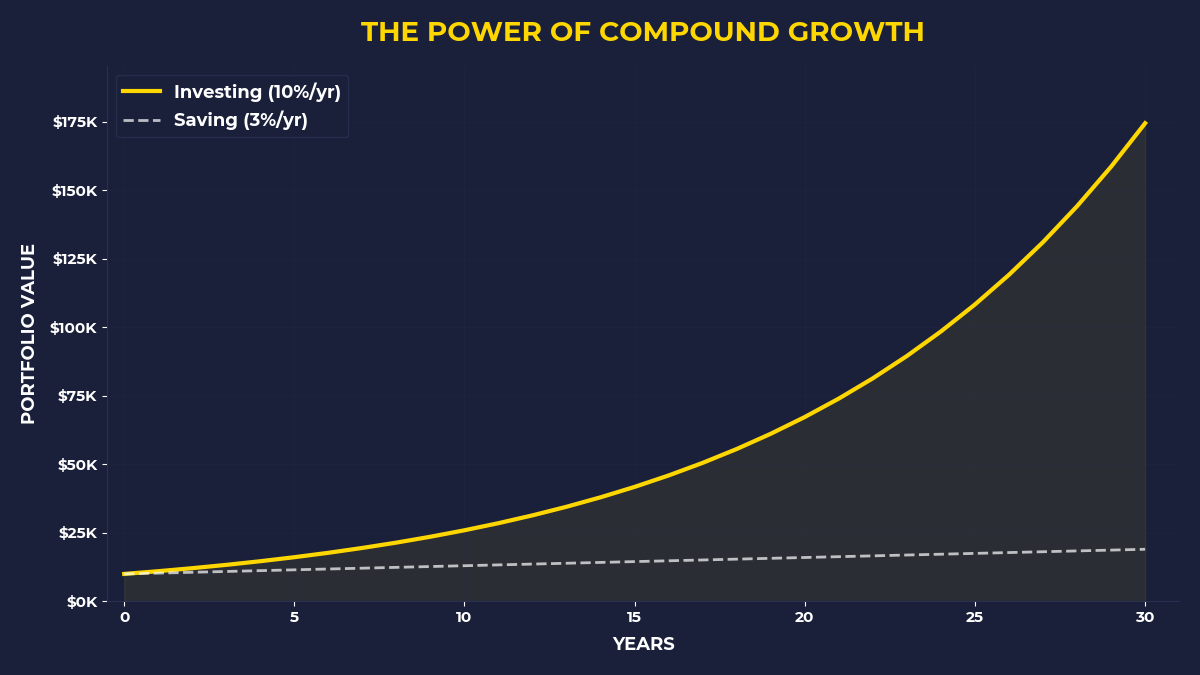

But 89% of individual investors who try to time markets underperform simple buy-and-hold strategies over 10-year periods. Even professional fund managers struggle with timing.

The real contrarian insight? Time in the market beats timing the market, but only if you can get time in the market to begin with.

Marcus had been waiting three years for the “perfect entry point.” Three years of zero ownership while asset prices generally trended up. He missed more wealth creation by waiting than most people lose in actual market downturns.

True contrarian investing isn’t about market timing. It’s about life timing.

What Happened to Marcus

Six months after that late-night phone call, Marcus texted me a screenshot. His brokerage account: $1,847.

He’d started with that first uncomfortable $50 purchase. Then $100 the next month. Then $150. Not because he got a raise or found extra money lying around—because he flipped the script on bill paying.

He renegotiated his phone plan. Downgraded his apartment. Sold his car and bought a cheaper one. Cut subscriptions. Each cost-cutting victory got reinvested into assets.

But the real transformation wasn’t the $1,847. It was the mental shift. Marcus stopped thinking like someone who works for money and started thinking like someone who owns things that generate money.

He was becoming a capital owner.

The One Thing to Remember

Contrarian investing isn’t about being smarter than other investors—it’s about being fundamentally different from other consumers. While everyone else prioritizes paying bills, you prioritize buying assets. While everyone else sends their cash to capital owners first, you become a capital owner first. The real contrarian move is flipping the order of your financial priorities, not timing market crashes.

If you take one action from this post:

• Move $50 to a brokerage account before paying any bills this month

• Buy any diversified stock or ETF with that money

• Figure out how to cover that $50 gap without touching the investment

🎬 Prefer watching? Check out the video version on YouTube: