Marcus — 29, software engineer in Denver — stared at his laptop screen at 11:47 PM on a Tuesday, watching his checking account balance drop from $3,200 to $1,850 in thirty-seven seconds. Rent: $1,350. Gone. Just like that.

He closed the laptop and walked to his kitchen, where seventeen other bills sat in a neat stack. Electric. Internet. Car payment. Insurance. Netflix. Spotify. His gym membership. All of them asking for his money. All of them owned by someone else.

The Invoice That Changed Everything

I know exactly how Marcus felt because three years ago, I was him.

Sitting in my own apartment, watching my own money disappear to my own stack of bills, when something clicked. I picked up my rent check — $1,100 to some property management company in another state — and realized something that should have been obvious but somehow wasn’t.

This wasn’t a bill. It was an invoice.

My landlord owned something I needed every single day. Four walls, a roof, an address where packages could find me. I needed it. He owned it. Every month, like clockwork, my demand became his cash flow.

Then I looked at the other sixteen bills.

The electric company owned the infrastructure that kept my lights on. I needed it. They owned it. My demand became their cash flow.

Verizon owned the network that connected my phone to the world. I needed it. They owned it. My demand became their cash flow.

Toyota Financial owned the loan on the car that got me to work. I needed it. They owned it. My demand became their cash flow.

Seventeen times a month, I was sending money to people who owned what I needed.

What Capital Actually Is

Here’s what I figured out that night: capital isn’t money sitting in a bank account.

Capital is stored demand.

When people need what you own, you have capital. When you need what other people own, you’re sending them capital. It’s that simple.

My friend Sarah — 31, marketing manager at a tech startup — called me last month, frustrated. “I make $78,000 a year,” she said. “Where does all of it go?”

I asked her to grab her phone and open her banking app. We went through her automatic payments together.

Rent: $1,400. Car payment: $380. Insurance: $145. Groceries: $320. Utilities: $90. Internet: $65. Phone: $85. Netflix, Spotify, Adobe, her yoga studio membership. Seventeen automatic payments to seventeen different capital owners.

“Sarah,” I said, “you’re not broke because you don’t make enough money. You’re broke because every dollar you earn has a capital owner already waiting for it.”

She went quiet for a long time.

The Two-Sided Game You’re Already Playing

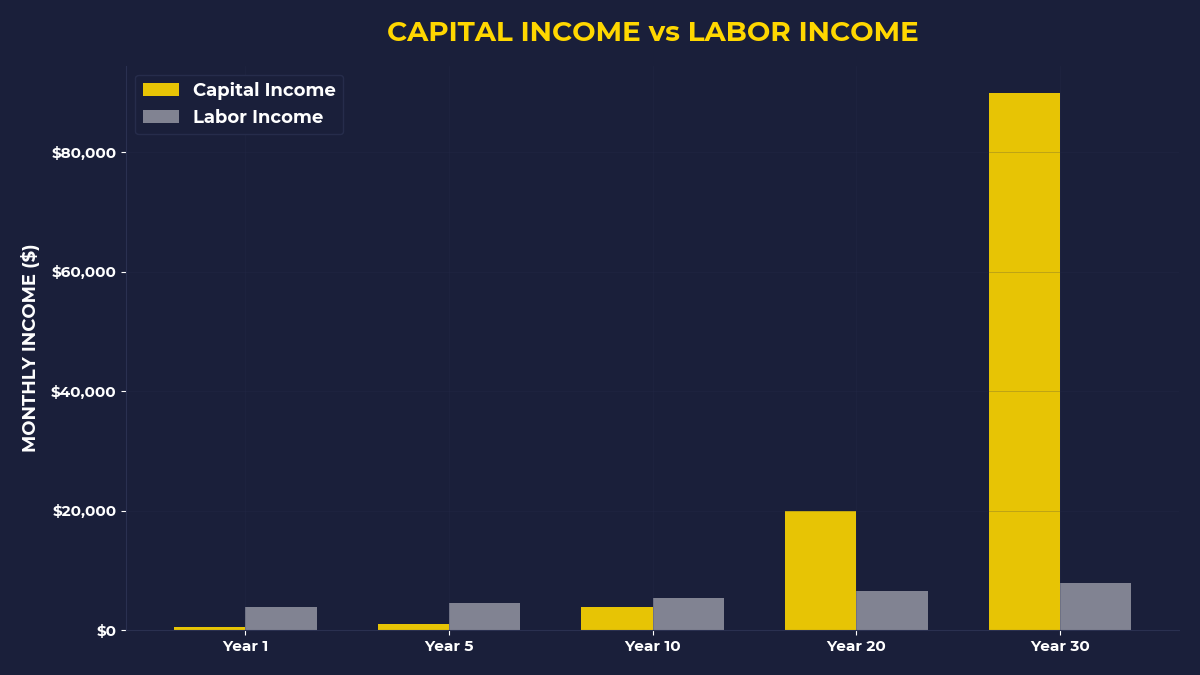

Most people think building wealth is about making more money. But Warren Buffett figured out something different when he was twelve years old, collecting lost golf balls around Omaha country clubs.

Young Warren would fish golf balls out of ponds and bushes, clean them up, and sell them back to golfers for 6 cents each. But here’s the part that matters: he didn’t keep doing the work forever.

He took the money from selling golf balls and bought more assets that people needed. A pinball machine. Then another. Then farmland. Then rental properties. Each one generated cash flow while he slept.

The golf ball business taught him the fundamental truth: there are two sides to every economic transaction. Someone owns what’s needed. Someone needs what’s owned.

The goal isn’t to work harder. The goal is to switch sides.

Why Famous Singers Get Rich While You Get Bills

You ever wonder why Taylor Swift makes $92 million a year while your accountant friend Jake — who’s honestly way better with numbers — makes $65,000?

It’s not because Taylor works harder. It’s because 50 million people demand what Taylor owns. Her voice. Her songs. Her brand. She owns the thing people want.

Jake sells his time. One hour equals one billable hour. He can’t sell the same hour twice.

Taylor sells ownership. One song gets bought by millions of people. She sells the same asset infinite times.

That’s the difference between labor and capital.

The Question Nobody Teaches You to Ask

Most financial advice asks: “What should you do to make more money?”

Get a promotion. Learn new skills. Start a side hustle. Work weekends. Grind harder.

But here’s what wealthy people ask instead: “What should I buy?”

Not “How can I work more hours?” but “What asset generates cash flow while I sleep?”

Not “How can I get a raise?” but “What do people need that I can own a piece of?”

I learned this lesson the expensive way. Two years ago, I was working 50-hour weeks at a consulting firm, making decent money but always feeling behind. I was asking the wrong question.

Then I met David Chen, a guy who owns three laundromats in Phoenix. David works maybe 15 hours a week. His laundromats generate $8,400 a month in cash flow while he’s at the beach with his kids.

“People always need clean clothes,” David told me. “I don’t do the washing. The machines do the work. I just own the thing people need.”

David bought demand. I was selling time.

Your Paycheck Is Already Spoken For

Look at your bank account right now. How much of next month’s paycheck is already committed to someone else’s capital?

If you’re like most people, 73% of your income is gone before you even see it.

Your rent or mortgage payment? That’s going to someone who owns real estate.

Your car payment? That’s going to someone who owns debt.

Your grocery bill? That’s going to companies that own food distribution.

Your Netflix subscription? That’s going to shareholders who own content.

Every month, you’re working to fund other people’s capital. The only question is: when do you start buying your own?

The Uncomfortable Truth About Building Wealth

Here’s what I wish someone had told me when I was 25: building wealth requires buying assets before you feel comfortable buying assets.

Most people pay their bills first, then invest whatever’s left over. But here’s the thing — there’s never anything left over.

The real game is this: buy assets first, then figure out how to pay the bills.

I know how that sounds. Reckless. Irresponsible. But think about it differently.

When your rent is due, you find a way to pay it, right? You don’t just shrug and become homeless. You prioritize it. You make it happen.

What if you treated building capital the same way?

The One Thing Most People Never Realize

Capital isn’t just money you invest. Capital is anything that converts other people’s needs into your cash flow.

A rental property is capital because people need housing.

Dividend-paying stocks are capital because you own pieces of companies people need.

A blog with 50,000 readers is capital because companies need attention.

A skill that saves people time is capital because people need efficiency.

The question isn’t whether you can afford to buy capital. The question is whether you can afford not to.

Every month you don’t own assets is another month you’re working to pay other people’s mortgages, fund other people’s retirements, and build other people’s wealth.

If You’re Someone Who Feels Stuck

If you’re reading this and thinking “This sounds great, but I barely have enough to cover my current bills” — I get it.

You’re not looking for another lecture about cutting out your daily coffee. You need a different approach entirely.

You need to start thinking like Harry Larson, the guy Warren Buffett read about as a kid. Harry saw a coin-operated scale at a drugstore, noticed how many people used it, asked the owner about the revenue split, and then bought seven more scales with the profits from the first one.

Harry asked: “What do people need that I can own?”

You can ask the same question, even if you’re starting with $50.

The One Thing To Remember

Your monthly bills aren’t just expenses — they’re proof that someone else figured out capital before you did. Every automatic payment from your account is automatic income to their account. The only way this changes is when you stop asking “How do I make more money?” and start asking “What should I buy that other people need?”

Here’s what to do next:

• Before you pay any bill this month, move $50 into a brokerage account and buy shares of an S&P 500 index fund — you’re buying pieces of companies that people need every day

• Look at your three biggest monthly payments and ask: “How could I own the thing I’m renting instead of rent the thing someone else owns?”

• Write down one asset you could buy in the next 12 months that would generate $25 per month in passive income — then start working backward to make it happen

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.