The $2,400 Question

Sarah — 29, marketing coordinator in Denver — stared at her savings account last Thursday morning. $2,400. The same amount that had been sitting there for eight months.

She’d read about investing. She’d downloaded three different apps. She’d bookmarked seventeen articles about index funds and watched YouTube videos until 2 AM. But every time she got close to clicking “buy,” something stopped her.

What if the market crashed the day after she invested? What if she picked the wrong stock? What if she needed that money for an emergency? The questions multiplied like rabbits, and her finger would hover over the “back” button until she closed the app entirely.

Meanwhile, her $2,400 earned $0.50 per month in her savings account. Wells Fargo, however, was lending that exact money to someone else at 7.2% interest.

Sarah’s anxiety was generating wealth. Just not for Sarah.

I Used to Be Sarah

I know exactly how she felt because I was paralyzed by the same fears for three years. From 2015 to 2018, I kept $12,000 in a checking account earning nothing while I “researched” investing. I read books, listened to podcasts, and joined Reddit forums about personal finance.

Here’s the thing. I wasn’t researching. I was procrastinating.

Every behavioral finance study in the world was playing out in my brain. Loss aversion — the fear of losing money outweighing the potential to gain it. Analysis paralysis — having so many options that I chose none. Status quo bias — sticking with the familiar even when it was clearly wrong.

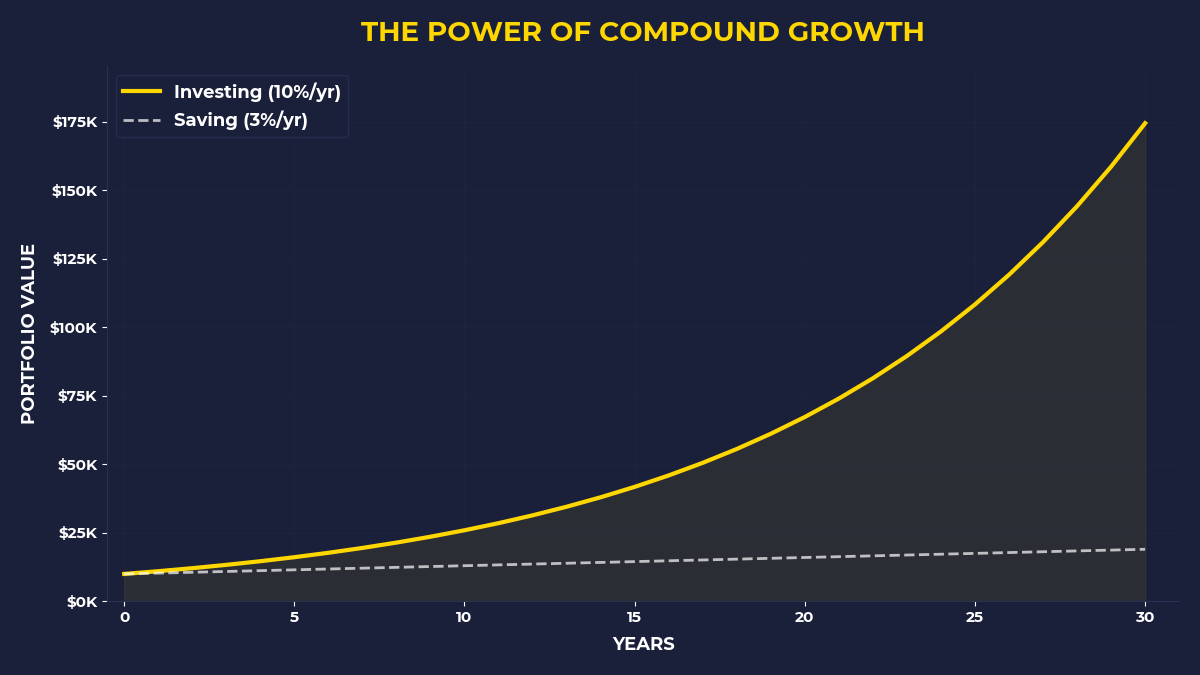

But I didn’t understand the real cost until I did the math later. That $12,000, invested in a basic S&P 500 index fund during those three years, would have grown to about $18,500. Instead, it earned maybe $36 in interest.

My psychological barriers to investing cost me $6,500. And that’s just the beginning — compound interest means I’m still losing money on that decision today.

The Fear Factory

Why does this happen to almost everyone? Your brain is running software designed for survival in a world that no longer exists.

Ten thousand years ago, if you made a bad decision about food or shelter, you died. So your ancestors who survived were the ones whose brains screamed warnings about every risk, no matter how small. Those anxiety-driven brains got passed down to us.

But here’s where it gets interesting. The people who profit from your money — banks, credit card companies, financial institutions — have spent billions studying these exact psychological triggers.

They know you’re afraid of losing money, so they offer “safe” savings accounts with 0.01% returns while they invest your deposits at 8-12% annual returns. They know you’re overwhelmed by choices, so they present investing as impossibly complex while keeping your money parked in their profitable products.

Your behavioral finance psychology isn’t a bug in the system. It’s a feature. For them.

The $47 Coffee Experiment

Let me show you how this works in practice. My friend Mike — 31, software engineer — told me this story last month that perfectly illustrates the psychological barriers to investing.

Mike buys a $5.50 latte every workday. That’s $27.50 per week, roughly $1,430 per year. He doesn’t think twice about it. But when I suggested he invest $50 per month in index funds, he immediately started calculating risks.

“What if I need that money?” he asked. “What if the market goes down right after I buy?”

Think about that. He’s completely comfortable spending $1,430 on coffee — money that’s gone forever — but terrified of investing $600 in assets that historically gain 10% annually.

This is loss aversion in action. The potential loss feels more real than the guaranteed loss. Meanwhile, Starbucks stock has returned 21% annually over the past decade.

Mike’s fear-based financial behavior was literally transferring his wealth to the shareholders of the companies he bought from, while keeping him out of the wealth-building game entirely.

What Nobody Tells You About Emergency Funds

Here’s the thing that changed my perspective entirely: I realized my “emergency fund” was actually an anxiety fund.

I kept $15,000 in savings “for emergencies.” But when I looked at my spending over five years, my actual emergencies — car repair, medical bills, job loss — totaled maybe $3,200. The other $11,800 was just sitting there, making me feel safe while earning nothing.

That $11,800 could have been working. If I’d invested it in 2018 and kept just $3,200 for real emergencies, I’d have an extra $8,000 today. Instead, I paid a $8,000 comfort tax to avoid feeling anxious about money.

Wild, right?

The banks and financial institutions love emergency fund advice because it keeps massive amounts of capital parked in their low-yield products. They’ve turned financial anxiety into their business model.

The Demand Recognition Shift

Everything changed when I stopped thinking about money and started thinking about demand.

Capital isn’t money sitting in accounts. Capital is stored demand. When you own shares of Microsoft, you own a piece of the demand for Windows, Office, and Azure. When you own Apple stock, you own a tiny slice of the demand for iPhones, MacBooks, and App Store purchases.

Every time someone buys a latte at Starbucks, pays for Netflix, or orders something on Amazon, they’re sending their cash to capital owners. The only question is: Are you sending or receiving?

This reframe eliminated most of my investing anxiety. I wasn’t gambling on price movements. I was buying ownership in the demand that already existed around me.

Sarah from the opening story? When she finally invested her $2,400 in a broad market index fund six months ago, she wasn’t betting on the market going up. She was positioning herself to receive payments from the economic activity happening every single day.

The Compound Anxiety Problem

Do you know what’s actually risky? Staying broke.

While you’re afraid of losing money in the market, inflation is guaranteed to reduce your purchasing power by 2-3% every year. That “safe” money is becoming less valuable every single month.

Meanwhile, the companies you buy from every day — Amazon, Apple, Google, Microsoft — are using your spending to generate returns for their shareholders. Your grocery bill becomes their dividend payments. Your Netflix subscription becomes their share buyback programs.

The psychological barriers to investing aren’t protecting you from risk. They’re guaranteeing that other people get rich from your economic activity while you stay on the payment side of capitalism.

That $2,400 in Sarah’s savings account? It’s not sitting idle. Wells Fargo is lending it to homebuyers at 7% interest, businesses at 8% interest, and credit card users at 24% interest. The bank’s shareholders collect the profits while Sarah gets anxious about risking her money in the stock market.

If You’re Ready to Stop Funding Other People’s Wealth

This post is for someone who recognizes themselves in Sarah’s story. You’re not broke, but you’re not building wealth either. You have some money saved, but it’s not working for you. You’ve been meaning to invest for months or years, but something always stops you.

You’re tired of feeling like everyone else is getting ahead while you’re stuck researching instead of acting.

The behavioral finance research is clear: time in the market beats timing the market, but only if you actually get in the market. Every month you spend optimizing is a month you’re not compounding.

The One Thing to Remember

Your money anxiety is a feature, not a bug — it’s designed to keep your capital flowing to people who already own assets instead of building your own ownership position. The companies profiting from your spending don’t share your psychological barriers to investing. They invest your payments immediately and automatically. The gap between your caution and their action is where wealth transfers happen.

- Tonight, open a brokerage account with Fidelity, Vanguard, or Schwab (takes 10 minutes)

- Tomorrow, invest $100 in VTI or VOO — not because it’s perfect, but because starting beats optimizing

- This weekend, calculate how much you spend monthly on subscriptions and services, then invest that exact amount in the companies you’re already paying

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.