Sarah’s $127 Problem

Sarah Martinez — 29, marketing coordinator in Phoenix — stared at her banking app on a Tuesday morning in March. $127 in checking. $2,400 on her credit card. Rent due in 8 days.

She’d been promoted six months earlier. Made $53,000 now instead of $47,000. But somehow, she felt broker than ever.

Her first instinct? The same one 97% of people have when money gets tight: “What else can I do to earn more?”

She started scrolling through side hustle articles. DoorDash. Upwork freelancing. Dog walking. Virtual assistant work. Maybe she could tutor high schoolers in Spanish on weekends.

Here’s the thing. Sarah was asking the wrong question entirely.

And so are you.

The Question I Wish Someone Had Asked Me

I know exactly how Sarah felt because I was 27 when I had my own version of that Tuesday morning panic. Different city, same bank balance anxiety. Same scramble for more income.

I spent two years asking “What should I do?” Downloaded every money app. Read productivity blogs. Optimized my morning routine. Applied for higher-paying jobs. Started a consulting side hustle that ate my weekends.

Made more money. Still felt broke.

Then my friend David — 34, UX designer in Austin — said something that rewired my brain completely. We were having beers after he’d just bought his second rental property.

“Most people ask what they should do for money,” he said. “Rich people ask what they should buy.”

I thought he was being pretentious. I was wrong.

Why Your Brain Tricks You Into Asking the Wrong Question

Your brain is programmed by 200,000 years of survival instinct. When resources get scarce, the ancient code kicks in: work harder, work longer, find more food.

In the modern economy, this translates to: get another job, work more hours, develop more skills, hustle harder.

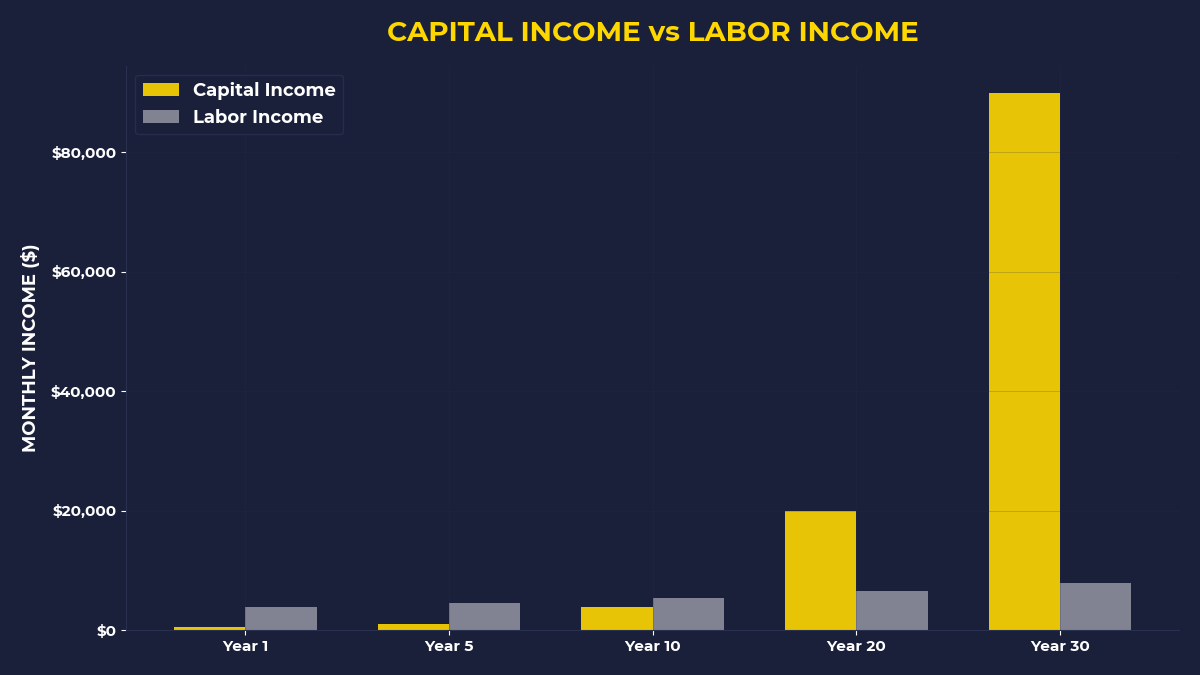

The problem? You’re playing a game that ended in 1850.

Today’s wealth isn’t built by trading more time for more money. It’s built by owning things that generate money while you sleep.

But here’s what your brain doesn’t understand: every successful person you admire stopped asking “What should I do?” and started asking “What should I buy?”

The Golf Ball Principle

Warren Buffett learned this lesson when he was 13 years old. He collected lost golf balls from water hazards and sold them for 6 cents each. Made decent money for a kid.

But here’s what made him different. When other kids would have pocketed the cash, Buffett asked: “What should I buy with this money?”

He bought his first stock at 11. Bought farmland as a teenager. Every dollar he earned went toward buying something that would generate more dollars.

Think about that. While his friends were asking “How can I make more money picking up golf balls?”, Buffett was asking “What can I buy that will make money without me?”

Different question. Different life.

What Sarah Discovered

Back to Sarah and her $127 problem. She called me three weeks after that panicked Tuesday morning.

“I did something crazy,” she said. “Instead of looking for a side hustle, I bought $100 of NVDA stock.”

I nearly choked on my coffee. “You had $127 total and you spent $100 on stock?”

“I know, I know. It sounds insane. But I kept thinking about what you said about asking the wrong questions.”

She scraped together rent money by selling some old furniture and picking up one freelance project. Not fun, but she managed.

Here’s what happened next. That $100 became $180 over the following months. More importantly, Sarah’s brain started rewiring itself.

Every paycheck, she asked herself: “What should I buy?” before paying any bills. Sometimes it was $50 of stock. Sometimes a $25 investment in her 401k. Once, she bought a $200 domain name for a business idea.

The amounts were tiny. The mindset shift was massive.

The Invoice Reality Check

Want to see why this question matters so much? Look at last month’s bills.

Rent or mortgage payment — that’s an invoice from a property owner. Car payment — invoice from a capital owner. Insurance premiums — invoice from shareholders. Groceries — invoice from food company owners. Netflix subscription — invoice from entertainment company owners.

Every single day, you send your cash to capital owners.

The question is: when do you switch sides?

People who stay broke forever keep asking “How can I pay these bills faster?” People who build wealth ask “How can I own the companies sending me these bills?”

The Compound Effect of the Right Question

Remember Harry Larson from the 1930s? He saw someone use a coin-operated scale at a drugstore. Instead of thinking “That’s a neat invention,” he asked: “What would it cost to buy one of those?”

Turned out the store owner paid $175 for the scale and kept 75% of the revenue. Harry bought his first scale with $175 from his savings account. Made $98 the first month.

But here’s the part that changed his life forever: instead of spending that $98, he asked again: “What should I buy?”

He bought another scale. Then another. Eventually owned 70 scales across town, generating $1,750 monthly in 1930s dollars — all from machines doing the work.

Same principle works today. Just different assets.

Your Capital vs. Everyone Else’s Capital

Look, maybe you can’t buy 70 coin-operated scales. But you can buy fractional shares of companies that operate thousands of machines worldwide.

Maybe you can’t start a rental property empire. But you can buy REITs that own thousands of properties.

Maybe you can’t build the next Netflix. But you can own a piece of Netflix.

The magic isn’t in the specific asset. It’s in consistently asking the right question: “What should I buy?” instead of “What should I do?”

Are You Someone Who’s Ready for This Shift?

This approach isn’t for everyone. If you’re looking for get-rich-quick schemes or investment tips that guarantee returns, keep scrolling.

This is for people who are tired of working harder just to send bigger checks to other people’s assets. People who want to own the things that generate income instead of just consuming them.

People who understand that building wealth isn’t about perfect timing or huge windfalls — it’s about rewiring your brain to think like a capital owner instead of a capital renter.

The One Thing to Remember

Every month, millions of people get their paychecks and immediately ask “What bills do I need to pay?” Meanwhile, a small group asks “What can I buy that will pay me?” The first group stays broke. The second group builds wealth. The only difference is the question they ask first.

Starting this month:

- Before paying any bill, move some amount — even $25 — into an investment account

- When you get unexpected money, ask “What should I buy?” before “What should I spend this on?”

- Replace “I need to make more money” thoughts with “I need to buy more assets” thoughts

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.