The Marketing Director Who Saw Her Future

Sarah — 31, marketing director at a mid-sized software company in Denver — got the email on a Tuesday morning in March. The subject line read “Exciting AI Integration Update.” Her stomach dropped before she even opened it.

The company had purchased an AI platform that could generate campaign copy, analyze customer data, and create social media content. “This will free up our team to focus on strategy,” the CEO wrote. Sarah knew exactly what that meant. Three of her five direct reports would be “transitioned out” within 90 days.

Here’s the thing that kept her awake that night: she realized she might be next.

The AI tool could do 80% of what her team did, faster and cheaper. Sure, someone still needed to “oversee strategy.” But did they need a $95,000-per-year director for that? Or would a $55,000 coordinator suffice?

I Watched This Movie Before

I know exactly how Sarah felt because I lived through something similar in 2019. Not with AI — with automation software that could handle most of the financial analysis I was doing as a consultant.

I remember sitting in my home office, watching a demo of software that could generate the same reports I spent 12 hours creating. The software did it in 47 minutes. And it never asked for vacation days or health insurance.

That moment changed everything for me. Not because I panicked — but because I finally understood what capital really means in the modern economy.

Most people think capital is money sitting in a bank account. It’s not.

Capital is stored demand. When people need what you own, you have capital. When people need what you do, you have a job. The difference matters more now than ever.

The Question Sarah Never Asked

Sarah spent the next three weeks polishing her resume and applying to similar positions. She was asking the wrong question entirely.

Instead of “How do I find another marketing director job?” she should have been asking “What should I buy to profit from this AI revolution?”

Think about what’s actually happening. Companies are spending billions on AI tools because those tools create massive efficiency gains. Every dollar a company saves on labor flows directly to capital owners — shareholders, private equity firms, venture capitalists.

Sarah was watching her industry get more profitable while her role became less valuable. She could either fight this trend or profit from it. Most people choose to fight.

They update their LinkedIn profiles instead of opening brokerage accounts.

The Real AI Economics Nobody Talks About

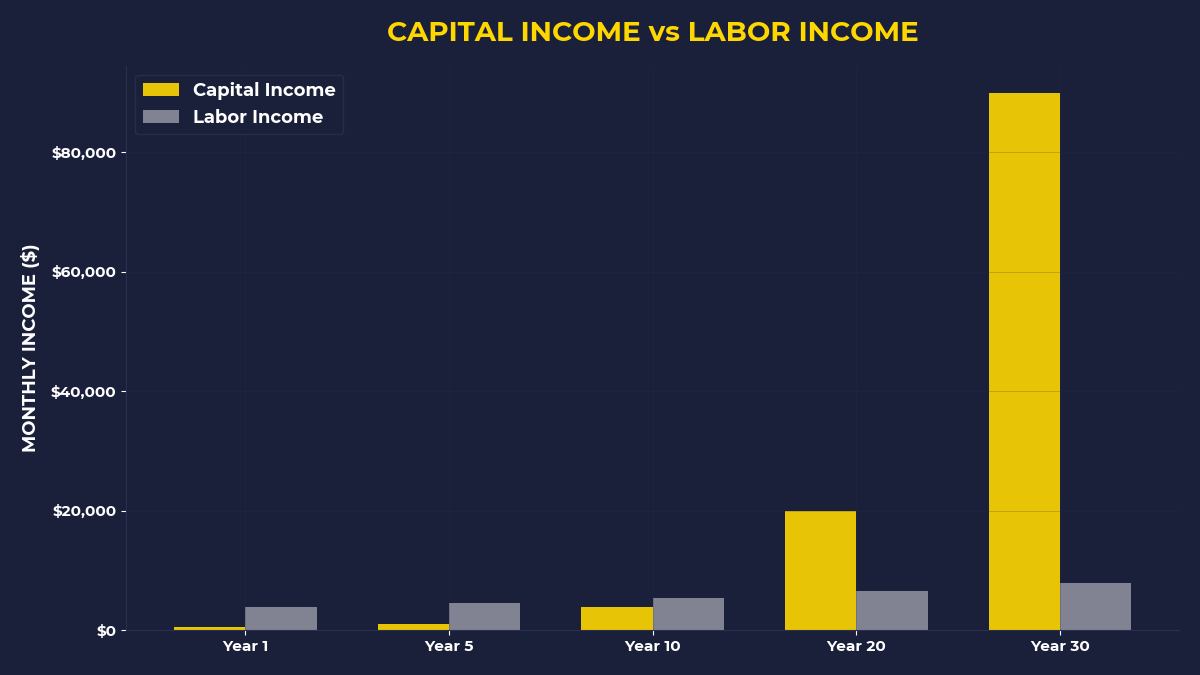

Here’s what’s actually happening with AI economics wealth building: We’re witnessing the largest transfer of value from labor to capital in modern history.

When a company replaces five $50,000 employees with a $30,000 AI subscription, that $220,000 in annual savings doesn’t disappear. It flows to whoever owns the company. If you own shares in that company, you get your piece of those savings. If you don’t, you just watch your industry shrink.

I learned this the hard way in my consulting days. The companies that bought automation software saw their profit margins jump 15-20% within six months. Their stock prices followed. Meanwhile, hundreds of consultants like me were scrambling for fewer, lower-paying contracts.

The pattern is always the same: technology increases productivity, productivity increases profits, profits flow to capital owners.

Labor gets disrupted. Capital gets richer.

Why Your Emergency Fund Is Making You Poorer

Do you have six months of expenses sitting in a savings account earning 0.5% interest? Congratulations — you’re funding the AI revolution for other people.

Every dollar you keep in “safe” cash is a dollar you’re not using to buy ownership in the companies profiting from artificial intelligence job displacement. While you’re playing defense, smart money is playing offense.

That $20,000 emergency fund earning $100 per year could have bought you shares in Microsoft, Nvidia, or Google — companies that have gained 40-60% value since AI started going mainstream. Instead, you’re letting inflation eat 8% of your purchasing power annually while telling yourself you’re being “responsible.”

Responsible for what? Staying poor?

The Sarah Update

Remember Sarah from Denver? Here’s what happened next.

Instead of just job hunting, she did something different. She took $15,000 from her savings account and bought shares in three AI companies and two index funds heavy in technology stocks. Not because she understood the tech — but because she understood the economics.

Companies were going to keep buying AI tools. Those tools were going to keep generating profits. Those profits had to go somewhere. She wanted to be on the receiving end for once.

Six months later, Sarah did get laid off. But something interesting happened. Her portfolio had grown by $3,800 during those same six months. Her emergency fund would have grown by $37.50.

More importantly, she’d shifted her mindset from “What job should I get?” to “What should I buy?”

The One Thing Most People Miss

The biggest mistake people make about AI investment opportunities for beginners is thinking they need to understand the technology. You don’t need to know how neural networks function to profit from them.

You just need to understand that AI makes businesses more profitable, and more profitable businesses reward their owners.

When Uber started using AI to optimize routes and pricing, drivers didn’t get richer. Uber shareholders did. When Netflix used AI to improve recommendations and reduce churn, content creators didn’t see bigger paychecks. Netflix investors did.

This pattern will repeat across every industry AI touches. Which is every industry.

The question isn’t whether AI will disrupt your job. It’s whether you’ll be on the ownership side or the labor side when it happens.

If You’re Someone Who Sees the Pattern

This post isn’t for people who think AI is just a fad or that their job is “too creative” to be automated. If you believe your skills are irreplaceable, stop reading. Keep polishing that resume.

This is for people like Sarah who see what’s coming and want to position themselves accordingly. People who understand that fighting technology is less profitable than owning it.

If you’re tired of watching other people get rich from changes that make your life harder, keep reading.

The One Thing To Remember

Every major technological shift creates two groups: those who own capital and those who depend on labor. AI is no different, except the shift is happening faster and more broadly than anything we’ve seen before. The companies integrating AI aren’t doing it to pay workers more — they’re doing it to pay workers less. Those savings flow to capital owners. You can either be one of them or keep sending them your paycheck every month through the products and services you buy.

Your action items for this week:

- Move 10% of your emergency fund into an index fund that includes major AI companies like QQQ or VTI

- Set up automatic investing so you buy more shares every month, regardless of your employment status

- Stop asking “How do I protect my job from AI?” and start asking “How do I profit from AI disrupting other people’s jobs?”

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.