Jessica — 29, marketing manager in Denver — sold her Apple stock in March 2020 for $63 a share.

She’d watched it drop from $80 to $63 in two weeks. The news was terrifying. Everyone was selling. Her gut screamed “get out before it gets worse.” So she did.

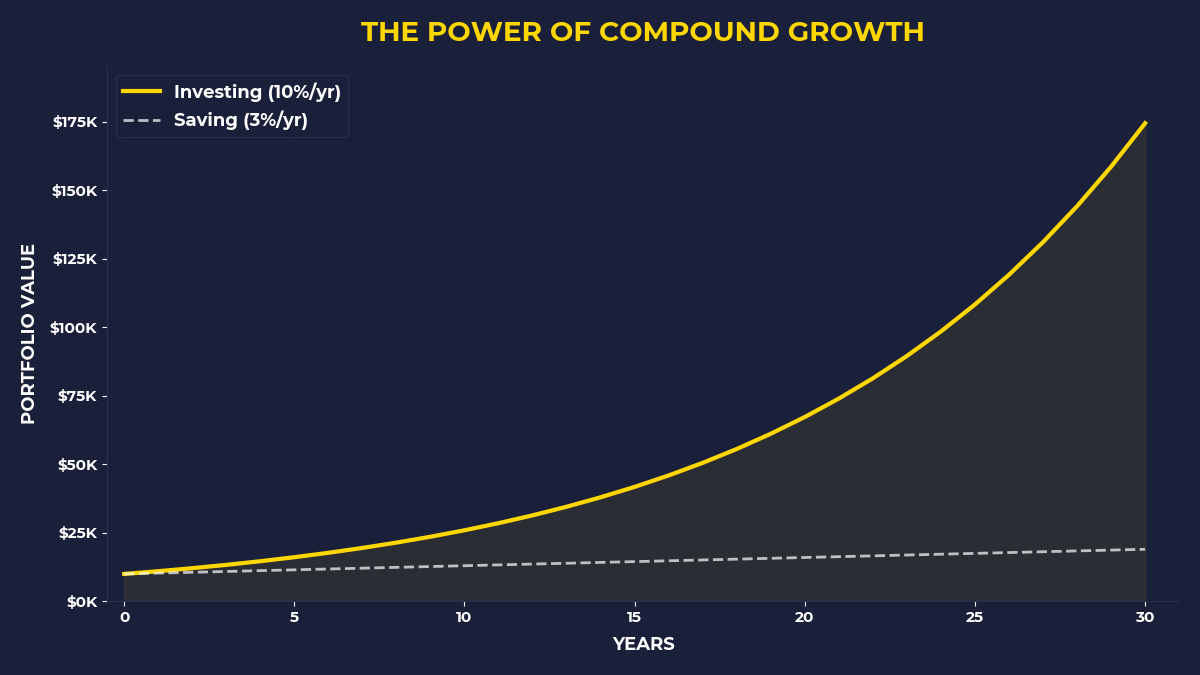

Apple hit $190 eighteen months later. Her $15,000 position would’ve been worth $45,000. But that’s not the real tragedy.

The real tragedy is what happened next. Jessica spent the next two years paralyzed, watching stocks climb while her cash earned 0.1% in savings. She’d check her old Apple position obsessively, calculating what she’d lost. By the time she finally got back in, the market had already doubled from those March 2020 lows.

She missed the entire recovery because her brain was protecting her from a danger that no longer existed.

Wild, right? The very mechanism designed to keep her alive was systematically destroying her wealth.

I Know Because I’ve Been There

I made the exact same mistake in 2008, just with different numbers.

I was 26, working at a small tech company, and I’d been putting $500 a month into index funds for three years. When Lehman Brothers collapsed and my portfolio dropped 40%, I panicked. Not just worried — actual panic. Heart racing, couldn’t sleep, checking my account every hour.

I sold everything in October 2008.

Here’s the thing. I knew, intellectually, that market crashes create buying opportunities. I’d read about 2001, 1987, 1929. I understood that selling low was the worst possible move.

But knowing and doing are completely different things when your lizard brain takes over.

That $18,000 I pulled out would be worth about $120,000 today if I’d just left it alone. But the real cost wasn’t the money — it was the five years I spent afraid to get back in, convinced the next crash was always coming.

The market recovered. I didn’t.

Your Stone Age Brain in a Digital Age Economy

Here’s what nobody tells you about behavioral finance: Your brain is literally working against your best interests.

Evolution wired us for immediate physical threats. See tiger, run fast, stay alive. This system worked perfectly for 200,000 years of human history. But it’s a disaster for building wealth in modern markets.

Think about it. Your ancestors never had to decide whether to hold a declining asset for potential future gains. They never had to ignore crowd behavior when their survival depended on group acceptance. They never had to delay gratification for decades while watching numbers on a screen.

Your brain treats a portfolio decline like a saber-tooth tiger attack. Fight, flight, or freeze.

Jessica chose flight. I chose flight. Most people choose flight.

The wealthy choose something else entirely.

The Pattern You Can’t See From Inside

Want to know the difference between wealthy people and everyone else? It’s not intelligence, education, or even starting capital.

It’s this: Wealthy people have learned to recognize their own behavioral finance traps before they spring them.

Let me show you the pattern most people never see. You make a smart financial decision — buy index funds, start a side business, invest in real estate. Things go well for a while. You feel clever.

Then something goes wrong. Markets drop. Business slows down. Property values decline. Your brain immediately starts the same script: “I knew this was too good to be true. I should get out while I can still salvage something.”

So you sell. You quit. You retreat to “safety.”

Then — and this is the cruel part — conditions improve. The asset recovers. The business opportunity was real. You watch from the sidelines as others profit from exactly what you abandoned.

This isn’t bad luck. This is your evolutionary wiring systematically transferring your wealth to people who’ve learned to override it.

The Loss Aversion Trap

Behavioral economists have a name for Jessica’s mistake: loss aversion. We feel losses about 2.5 times more intensely than equivalent gains. Losing $1,000 hurts more than gaining $1,000 feels good.

This made sense when losing your winter food store meant death. But in modern markets, this bias is a wealth destroyer.

Here’s how it plays out in real life. You buy a stock at $100. It drops to $80. You feel terrible — not just disappointed, but genuinely distressed. Your brain screams “Stop the bleeding!” so you sell.

But now you need that same stock to hit $125 for you to feel as good about buying as you felt bad about selling at $80. So you wait. And wait. And wait.

Meanwhile, people who understand this trap are buying at $80, knowing your pain is their opportunity.

Every market crash is the same story: Millions of people selling their future wealth to the few who’ve learned to think differently.

The Herding Instinct That Keeps You Poor

Remember how Jessica sold because “everyone was selling”? That’s not weakness — that’s 200,000 years of evolution.

Our ancestors survived by staying with the group. Being wrong with everyone else was safer than being right alone. If the tribe ran from a noise in the bushes, you ran too. Better to waste energy than become dinner.

But in markets, this instinct is poison.

When everyone’s selling, prices are low — that’s when you want to buy. When everyone’s buying, prices are high — that’s when you want to be cautious. The crowd is almost always wrong at turning points.

Yet your brain makes you feel physically uncomfortable doing the opposite of the crowd. Your nervous system treats contrarian investing like social exile.

I’ve learned to recognize this feeling. When every financial news headline makes me want to sell, when my friends are all talking about the same investment opportunity, when I feel stupid for not following the crowd — that’s when I know I’m probably onto something valuable.

The discomfort isn’t a warning. It’s a signal.

The Recency Bias That Steals Your Future

Here’s another trap I fell into hard: assuming the recent past predicts the future.

After I sold in 2008, I spent years convinced the next crash was imminent. Every market rally felt like a setup. Every piece of bad news felt like confirmation that I’d been smart to get out.

This is recency bias — giving too much weight to recent events. Your brain treats the last thing that happened as the most likely thing to happen next.

But markets don’t work that way. Crashes don’t predict more crashes. Bull markets don’t predict more bull markets. What feels most likely is often least likely.

The people who got rich from the 2008 crash weren’t the ones predicting it. They were the ones who bought when everyone else was selling, even though it felt insane at the time.

The One Question That Changes Everything

What if you could short-circuit these behavioral finance traps before they spring?

I’ve found one question that works better than any other: “What would I do if I couldn’t check the price for five years?”

This question forces you past the emotional noise. It makes you think about fundamentals instead of price movements. It connects you to the original reason you made the investment.

When Jessica was watching Apple drop in March 2020, this question would’ve changed everything. Would she have sold Apple stock if she couldn’t check the price until 2025? Of course not. She’d have remembered why she bought it: because people aren’t going to stop using iPhones.

But our brains don’t naturally think this way. We’re wired for immediate response to immediate threats. Long-term thinking requires conscious effort to override our programming.

Every time I feel that familiar urge to “do something” about a declining position, I ask myself this question. Most of the time, the answer is: “I’d hold, probably buy more, and focus on other things.”

So that’s what I do.

The Automation Solution

Here’s what I’ve learned after 15 years of fighting my own behavioral biases: You can’t win through willpower alone.

Your rational mind makes plans. Your emotional mind makes decisions. And your emotional mind is stronger, faster, and more convincing than you think.

The solution isn’t better discipline. It’s better systems.

I now automate every investment decision I can. Money moves from my checking account to index funds every month, whether markets are up or down. I can’t stop it without jumping through hoops.

I’ve also learned to pre-commit to holding periods. Before I buy anything, I write down the minimum time I’ll hold it and the specific conditions that would make me sell. Not “if it drops 20%” — that’s just loss aversion in disguise. Real conditions, like “if the business model fundamentally changes.”

These aren’t perfect solutions. But they work better than hoping I’ll make rational decisions when my amygdala is firing.

The People This Post Is For

If you’re someone who’s made smart financial decisions only to sabotage them later — this post is for you.

If you’ve ever sold something at the worst possible time because it “felt right” — this post is for you.

If you’re tired of watching other people get rich from opportunities you abandoned — this post is for you.

But if you think you can beat markets through superior analysis or timing, this probably isn’t your fight yet. You need to lose money to emotional decisions before you’ll take behavioral finance seriously.

And that’s okay. I had to learn the hard way too.

The One Thing To Remember

Your brain isn’t broken — it’s just solving the wrong problem. Evolution optimized you for survival in small groups facing immediate physical threats. But building wealth requires exactly the opposite instincts: thinking long-term, acting against the crowd, and staying calm when everyone else panics. The wealthy aren’t smarter than you — they’ve just learned to recognize when their stone age wiring is about to cost them money.

Here’s what to do starting today:

• Set up automatic investing so your rational mind makes the decisions, not your emotional mind in crisis moments

• Write down your selling criteria before you buy anything — specific business conditions, not price movements

• Ask yourself “What would I do if I couldn’t check the price for five years?” before making any emotional financial decision

🎬 Prefer watching? Check out the video version on YouTube: