Marcus checked his account balance while standing in line at Whole Foods, cart full of organic everything. $847 left until payday. The groceries would cost $180. His rent was due in three days — $2,200. Car payment next week — $420. Student loans auto-drafting Friday — $340.

He’d just gotten a promotion to senior marketing manager at 29. Made $78,000 now. Felt broke anyway.

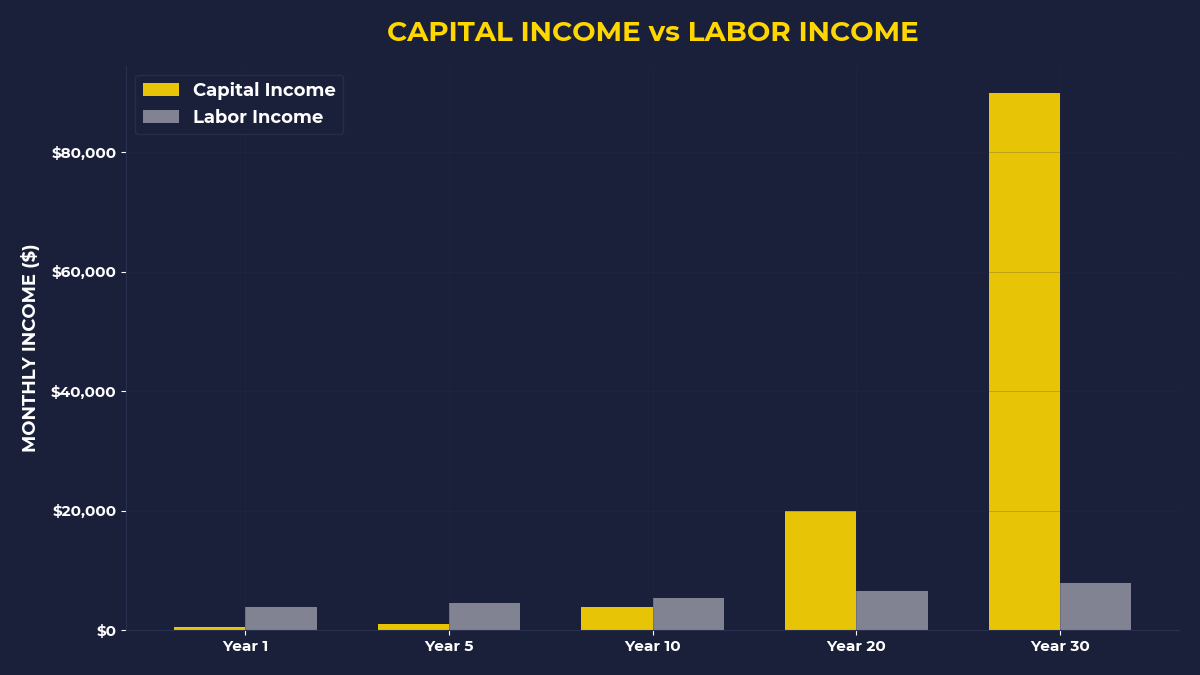

Marcus represents 73% of Americans living paycheck to paycheck, even with decent incomes. But here’s what makes his story different from every other broke professional story you’ve heard: Marcus thinks he’s a contrarian investor.

The Contrarian Delusion I Lived For Years

I know exactly how Marcus felt because I was him at 26.

I’d read every contrarian investing book. Bought stocks when others were selling. Held cash when everyone was buying. Felt intellectually superior watching my coworkers chase hot stocks while I built my “value portfolio.”

Here’s what I completely missed: true contrarian investing has nothing to do with which stocks you pick.

I was making the same fundamental error as 97% of people who think they’re contrarian investors. I was being contrarian in the market while following the crowd in my actual money flow. Every month, I sent my paycheck to other people’s capital first. Landlord got his cut. Credit card companies got theirs. Car company, insurance company, phone company — everyone got paid before I bought a single share of stock.

I was a fake contrarian. A contrarian cosplayer.

What Real Contrarian Investing Actually Looks Like

Real contrarian investing isn’t about buying unpopular stocks. It’s about doing the one thing 97% of people refuse to do with their money flow.

Think about that grocery store scene with Marcus. What would a real contrarian do?

The crowd pays bills first. Rent, groceries, car payment, Netflix, gym membership — everyone else gets their money before Marcus invests a dollar. That’s not just normal behavior. That’s literally what every financial advisor tells you to do. “Pay your bills, build an emergency fund, then think about investing.”

A real contrarian flips this completely.

Warren Buffett figured this out selling golf balls as a kid. He didn’t pay his expenses first, then invest what was left. He invested first, then figured out how to cover expenses. When he found lost golf balls and sold them for $6 per dozen, he didn’t spend that $6 on candy or comic books. He used it to buy more assets — pin-ball machines, farmland, eventually stocks.

Here’s the thing most people miss about Buffett’s early years: he lived in friends’ garages while building capital. He paid himself first, everyone else second. Even when it was uncomfortable. Especially then.

Why Your Payment Priority Reveals Everything

Every month, you get a paycheck. What happens in the next 72 hours reveals whether you’ll build wealth or stay broke forever.

The crowd follows this sequence: rent → groceries → car payment → insurance → utilities → credit cards → savings → maybe some investing if there’s anything left.

Contrarian investors reverse it: investing → bills → everything else.

I know what you’re thinking. “That’s impossible. I can’t pay rent with stock shares.” You’re right. But you’re also missing the point.

True contrarian investing psychology means you prioritize buying assets before paying other people’s assets. Even if it’s $50. Even if it makes the month tight. Even if you have to earn extra money to cover the bills you couldn’t pay because you invested first.

The Story Nobody Tells About Building Capital

Let me tell you about Robert Kiyosaki during his broke years. Most people know him from “Rich Dad Poor Dad.” What they don’t know is that he once lived in a friend’s car while building his first business.

When bill collectors called, when rent was overdue, when his wife wanted him to get a regular job — Kiyosaki had one rule: pay himself first. Every dollar that came in, he invested a portion in assets before paying anyone else.

The contrarian part wasn’t what assets he bought. The contrarian part was the order he bought them.

When people asked how he could invest while behind on bills, he’d work extra jobs. Mow lawns. Wash cars. Whatever it took to cover the bills he couldn’t pay because he’d already invested that money.

Wild, right?

Most people would call this financial suicide. Kiyosaki called it financial education.

Why This Feels Impossible (And Why That’s The Point)

Your brain is wired to pay survival expenses first. Shelter, food, transportation — these feel like life-or-death priorities. They trigger ancient programming that says “secure survival first, think about growth later.”

This is exactly why contrarian investing psychology is so powerful. And so rare.

99% of people follow their survival programming. Pay the rent. Buy groceries. Cover the car payment. Send money to all the capital owners first, then maybe — maybe — buy some capital for themselves if there’s anything left.

The 1% who build significant wealth flip this script. They buy capital first, then figure out how to survive. Not because they’re reckless. Because they understand something the crowd doesn’t: building capital is a survival skill, not a luxury.

The $50 Test That Reveals Your True Investing Psychology

Here’s how you know if you’re actually a contrarian investor or just playing dress-up:

Next paycheck, before you pay any bill, transfer $50 to a brokerage account. Buy $50 worth of an S&P 500 index fund. Then pay your bills.

Can’t do it? You’re not a contrarian investor. You’re a crowd follower who happens to pick different stocks.

The amount doesn’t matter. It could be $20. It could be $200. What matters is the sequence. Capital first. Everything else second.

This isn’t about the money. It’s about rewiring your financial psychology. Teaching your brain that building capital isn’t something you do with leftover money. It’s something you do with first money.

Why Everyone Gets Your Money Before You Do

Look at your bank account right now. How much went to capital owners this month versus how much went to building your own capital?

Your landlord owns real estate. You pay him $2,200.

Credit card companies own debt instruments. You pay them $340.

Netflix owns entertainment content. You pay them $15.

The grocery store owns food distribution. You pay them $600.

Add it up. Thousands of dollars every month flowing from your paycheck to other people’s capital. And at the end of the month, you invest whatever’s left — usually nothing.

This is the opposite of contrarian investing psychology.

True contrarians understand that every dollar sent to a capital owner is a dollar not building your own capital base. They don’t avoid necessary expenses. They just refuse to send 100% of their cash flow to other people’s assets before buying their own.

The One Thing To Remember

Contrarian investing isn’t about finding unpopular stocks or timing market crashes. It’s about reversing the cash flow priority that keeps 97% of people sending their paychecks to capital owners their entire lives. When you pay yourself first — even $50, even when it’s uncomfortable — you’re practicing the most contrarian financial behavior possible: building your own capital instead of everyone else’s.

• Before paying any bill this month, transfer money to buy assets first

• If this makes bills tight, find extra income to cover what you can’t pay

• Repeat every month until investing first feels as natural as paying rent first

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.