Sarah — 29, marketing manager in Denver — called me at 7:23 AM on a Tuesday. I could hear her coffee machine grinding in the background.

“I just calculated something,” she said. “If I keep investing the way I’m supposed to, I’ll have enough to retire when I’m 67. Maybe 65 if the markets are good.”

Pause.

“I’ll have worked 45 years to buy 15 years of freedom.”

That’s when she started crying. Not the dramatic kind — the exhausted kind that comes when you realize the game is rigged and you’ve been playing by their rules.

I Know Exactly How Sarah Felt

Because I was there too. At 26, I had a retirement account, a savings account, and a five-year plan that made my parents proud. I was following every piece of investment advice I’d ever heard: max out the 401k, build an emergency fund, invest in low-cost index funds.

The math looked good on paper. 7% annual returns compounded over 40 years. The magic of compound interest would make me a millionaire by retirement.

But something bothered me about that timeline. Forty years of trading my days for dollars, just to afford the years when my body would be too worn out to enjoy the money.

I remember sitting in my apartment, looking at my brokerage app, watching my portfolio creep up by $127 that month. My rent alone was $1,850.

That’s when it hit me: **I was optimizing for the wrong thing entirely.**

The Investment Philosophy Nobody Teaches

Most investment philosophy focuses on returns. How to get 8% instead of 6%. How to time the market. How to pick the right stocks or funds.

But here’s what Sarah and I both discovered: **the most successful investors don’t optimize for returns — they optimize for time freedom.**

Think about Warren Buffett’s early years. At age 11, he bought his first stock. But the real insight came when he started buying golf balls from the rough at local courses, cleaning them up, and reselling them in packs of 12 for $6.

He wasn’t chasing returns. He was buying himself out of hourly labor.

When he made enough money from golf balls, he bought a used car and rented it to a friend. When that generated cash flow, he bought farmland. Each purchase moved him further away from trading time for money.

The goal was never to optimize his hourly wage. The goal was to eliminate the need for hourly wages altogether.

Why Your Current Strategy Keeps You Trapped

Here’s the brutal truth about traditional investment philosophy: it assumes you’ll keep working for 40+ years.

Every financial advisor tells you to max out your 401k. Save 20% of your income. Invest in diversified index funds. Wait decades for compound interest to work its magic.

This isn’t investment advice — it’s retirement planning for people who accept that they’ll never own anything that pays them while they sleep.

Look at your monthly bills for 30 seconds. Rent to your landlord. Car payment to the bank. Phone bill to Verizon. Netflix to Reed Hastings’s shareholders. Coffee to Howard Schultz’s equity holders.

**Every month, you send cash to capital owners. The goal isn’t to send it more efficiently — it’s to switch sides.**

What Buying Time Freedom Actually Looks Like

Let me tell you about Marcus, a 24-year-old electrician I met last year. Instead of maxing out his 401k, he did something that made his parents panic.

Marcus took his first $5,000 and bought a used pressure washer and a pickup truck. He started cleaning driveways on weekends. Made about $300 per weekend.

Most people would call this a side hustle. Marcus called it buying himself 52 Saturday mornings per year.

Within eight months, he had enough cash flow to hire his younger brother. Now Marcus makes $300 every weekend without working weekends. He takes that $300 and buys shares in companies that other people work for.

His parents think he’s financially reckless. His retirement account is smaller than his college friends’. But Marcus owns something that generates cash flow while he sleeps.

That’s not a side hustle. That’s capital.

The Question That Changes Everything

Here’s the reframe that shifted everything for Sarah, Marcus, and me:

Instead of asking “What should I do to make money?” start asking “What should I buy to make money?”

The first question leads to jobs, side hustles, and trading time for dollars. The second question leads to equity ownership and compound returns through assets.

When Sarah called me that Tuesday morning, she was stuck in the “what should I do” mindset. She was optimizing her 401k contributions, reading investment books, planning to work harder for promotions.

Now she asks different questions: What asset can I buy this month? What equity position can I take? What system can I own instead of work for?

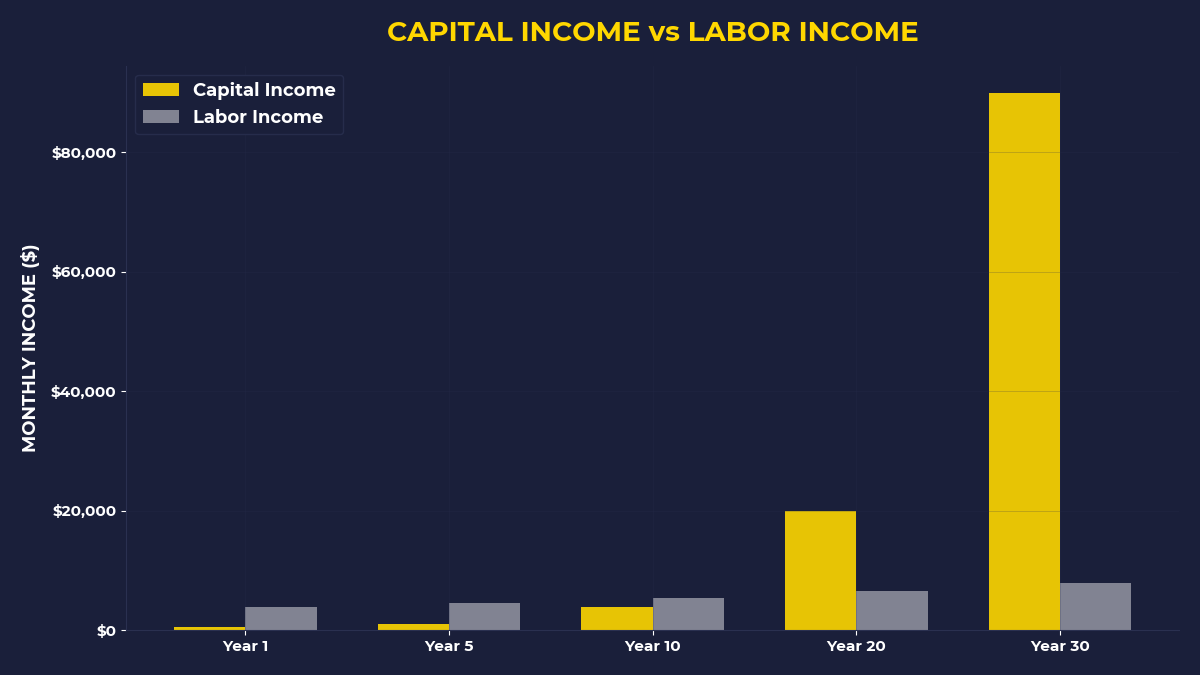

The Compound Returns Nobody Talks About

Traditional investing compounds your money. But building wealth through equity ownership compounds your time.

Every month that Marcus’s pressure washing business generates $1,200 without his labor, he gets 1,200 extra dollars AND 40 hours of his life back. He can use those 40 hours to find the next asset to buy.

Sarah started small. Instead of maxing her 401k, she put $800 a month into dividend-paying stocks. Not for the 3% yield — for the psychological shift. Every quarter, companies send her checks for owning pieces of their businesses.

It’s not about the money. It’s about rewiring her brain to think like an owner instead of an employee.

For People Who Want To Break Free

This investment philosophy isn’t for everyone. If you love your job and want to work until 67, keep maxing out that 401k. There’s nothing wrong with that path.

But if you’re someone who lies awake at night calculating how many years you have left… if you’re tired of sending your paycheck to other people’s equity positions… if you want to own something instead of just working for something…

Then stop optimizing for returns. Start optimizing for time freedom.

The One Thing To Remember

**Capital is stored demand, and your goal is to own pieces of things that people will always need.** Every dollar you spend on rent, food, transportation, and entertainment is demand that flows to capital owners. The fastest way to build wealth isn’t to earn more or invest better — it’s to gradually switch from sending cash to capital owners to becoming a capital owner yourself.

Here’s what to do this week:

• Before paying any bills this month, buy $100 worth of stock in a company you send money to regularly (your bank, your phone company, your grocery store)

• Ask yourself: “What asset could I buy with next month’s savings instead of putting it in index funds?”

• Find one thing you pay for monthly and research whether you could own equity in that business or category instead

🎬 Prefer watching? Check out the video version on YouTube: