Warren Buffett made more money picking up golf balls at age 11 than most adults make in their careers. Not because he found more balls. Because he understood something about capital that escapes 97% of investors even today.

Here’s what happened: Young Warren collected lost golf balls around Omaha courses, cleaned them up, and sold them in packs of 12 for $6. Standard hustle, right? Wrong. The genius was what he did next. He took every dollar from those sales and bought assets — first a pinball machine for $25, then farmland, then more cash-flowing businesses.

While other kids spent their money on candy and toys, Buffett was building what I call a demand capture system.

Most people think capital means money sitting in a bank account. That’s not capital. That’s just stored labor waiting to decay through inflation. Real capital is something entirely different — and once you see it, you can never unsee why everyone around you stays broke.

What I Learned From My Monthly Bills

I used to think I was managing my money well. I had a budget spreadsheet, emergency fund, even a 401k. Then one Tuesday morning, I sat down with a stack of bills and had an epiphany that changed everything.

Every single invoice was a payment to someone else’s capital.

My rent check? Payment to the landlord’s real estate capital. Netflix subscription? Payment to Reed Hastings’ content capital. Starbucks latte? Payment to Howard Schultz’s brand capital. Even the parking meter outside — payment to the city’s infrastructure capital.

I was funding everyone else’s demand capture systems while building none of my own.

Think about that. Your grocery bill, phone plan, car insurance, gym membership — every single dollar flows to someone who owns the thing that creates recurring demand. You’re not the customer. You’re the cash flow.

Capital Is Stored Demand, Not Stored Money

Here’s the insight that separates capital owners from everyone else: Capital isn’t money. Capital is a structure that stores and amplifies human demand over time.

When you buy Apple stock, you’re not buying a piece of paper. You’re buying a slice of humanity’s demand for smartphones, computers, and digital services. When that demand grows, your slice grows. When Apple creates new products that capture more demand, your ownership captures more value.

This is why famous singers make millions while equally talented street musicians stay poor. The singer owns the capital structure — recording contracts, distribution deals, brand recognition — that captures demand at scale. The street musician just creates labor that disappears the moment the performance ends.

Demand persists. Labor disappears.

Between 1990 and 2020, Coca-Cola’s revenue grew from $10.2 billion to $33 billion. Not because people got thirstier. Because Coke owns the capital structure that captures humanity’s demand for sweetened beverages across 200+ countries. Every sip, every bottle, every vending machine sale flows through their demand capture system.

Why Your Brain Keeps You Poor

Your primate brain is wired for immediate labor-for-reward exchanges. See threat, run fast, get safety. See opportunity, work hard, get food. This worked perfectly when humans lived in small tribes competing for scarce resources.

But capital theory for wealth building operates on compound timescales that your brain can’t process intuitively.

When Warren Buffett’s Berkshire Hathaway returned 20.1% annually from 1965 to 2021, most investors couldn’t stick with it. The stock fell 37% in 1974-1975. Down 49% in 2008. Your ancient brain screams “DANGER” during every drawdown and “SAFETY” during every bubble.

This is why 89% of active fund managers underperform the S&P 500 over 20 years. They’re not stupid. They’re human. They make decisions when fear spikes and greed peaks, exactly when capital owners should be doing the opposite.

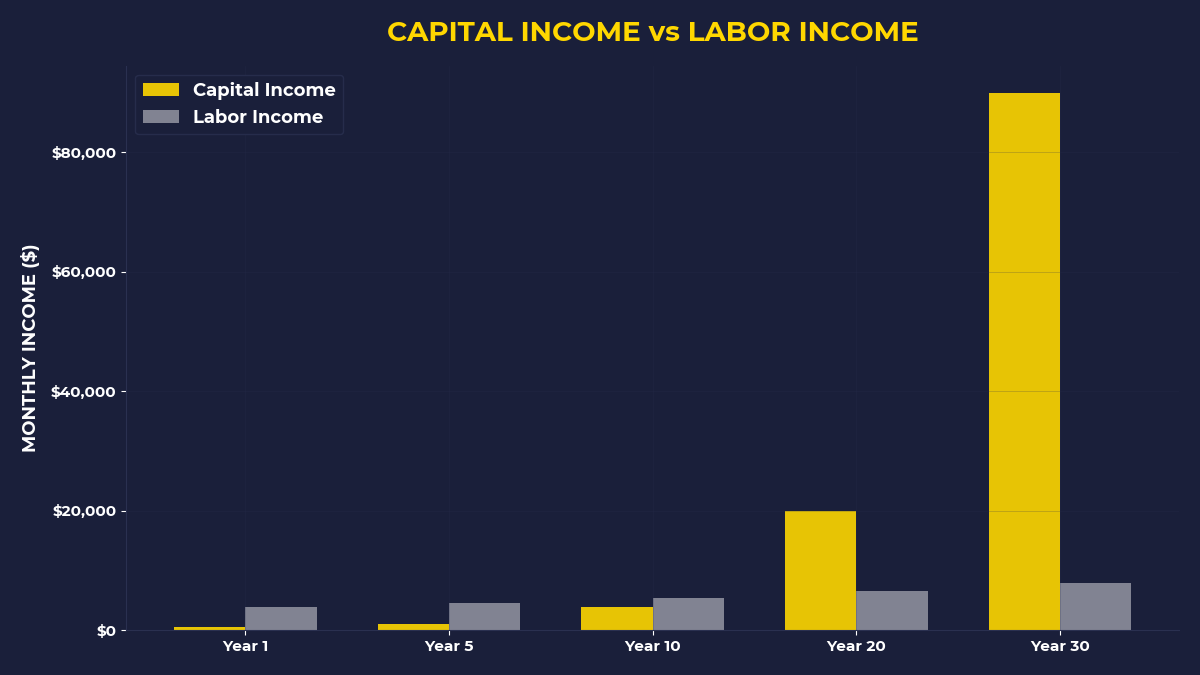

The Compound Interest Capital Accumulation System

Let me tell you about Harry Ralston’s weight scale empire. In the 1930s, Harry noticed people paying a penny to weigh themselves at a local drugstore. The owner told him the scale generated $20 monthly — 75% went to the scale company, 25% to the store.

Harry bought three scales for $175. Then something remarkable happened.

He used the coins from the first three scales to buy 67 more scales. Not with his job income. With the capital’s own output. By the time he finished, Harry owned 70 scales generating $1,750 monthly passive income in 1930s money — equivalent to about $30,000 today.

This is compound interest capital accumulation. You don’t just save money and hope it grows. You buy demand-generating assets, let them produce cash flow, then use that cash flow to buy more demand-generating assets.

The key insight: Harry wasn’t working 70 times harder than when he had one scale. The capital was working for him.

What Would Happen If You Stopped Creating Labor?

Most people approach wealth backwards. They ask: “What should I do to make money?” Capital owners ask: “What should I buy to capture demand?”

The difference is leverage.

When you create labor, your income scales linearly with your time. Work twice as hard, make twice as much. Work half as hard, make half as much. Hit the ceiling of human productivity, hit the ceiling of your wealth.

When you buy demand, your income scales with the compound growth of human desires. Own a piece of Microsoft, benefit from every business that needs software. Own a piece of Amazon, benefit from every person who wants convenience. Own a piece of Tesla, benefit from every driver who wants clean energy.

You’re not trading time for money. You’re trading money for ownership of time-independent cash flows.

The Lazy Investor’s Advantage

I once met a woman who inherited $50,000 and did absolutely nothing with it for 30 years except buy Vanguard’s S&P 500 index fund. No research, no stock picking, no market timing. Just automatic monthly investments of whatever she could spare.

That $50,000 became $1.2 million by 2023.

Meanwhile, her brother — an engineer who made $120,000 annually — spent those same 30 years optimizing his career, getting promotions, and saving diligently in savings accounts. He accumulated $180,000.

She owned demand. He created labor.

The S&P 500 averaged 11.8% annually during those 30 years because the companies inside it captured growing slices of human demand. Her ownership grew with that demand. His savings just sat there, earning 2% while inflation ate 3%.

This is why buying assets versus working harder isn’t even close. Assets compound. Labor just adds up.

If You’re Still Trading Time for Money

Look, I’m not saying quit your job tomorrow and become a day trader. That’s not buying demand — that’s creating a different kind of labor that’s even more exhausting.

But if you’re still asking “What should I do?” instead of “What should I buy?”, you’re thinking like someone who will always need to work.

Start small. Take 10% of your paycheck before you pay any bills. Yes, before. Buy an index fund that owns pieces of companies with sustainable demand. QQQ owns the top 100 tech companies. VTI owns the entire U.S. stock market. VXUS owns everything else.

You’re not picking stocks. You’re buying ownership of human demand itself.

When your rent check goes out, remember: you’re paying someone else’s capital. When your investment contribution goes out, remember: you’re building your own capital.

The goal isn’t to get rich quick. It’s to stop making other people rich while you stay poor.

What The Primal Investor Takes Away

• Capital is stored demand, not stored money — buy ownership of recurring human desires, not just cash that sits there

• Pay yourself first, bills second — invest 10% before any other expense to build your capital ownership systematically

• Ask “What should I buy?” not “What should I do?” — shift from creating labor to purchasing demand-capture systems

• Compound interest capital accumulation beats linear labor income — let assets buy more assets instead of trading time for money

• Your monthly bills are invoices from other people’s capital — every subscription and payment flows to someone else’s ownership structure

• Index funds let you own pieces of thousands of demand-generating businesses without picking individual stocks or timing markets

Your paycheck is someone else’s expense. Your capital is your own revenue stream. Choose wisely.

🎬 Prefer watching? Check out the video version on YouTube:

")