Sarah Martinez — 28, marketing manager in Denver — stared at her phone screen in the Starbucks parking lot last Tuesday morning. Her portfolio was down 18% in three weeks. She’d bought those growth stocks at their peak in January, riding the wave of everyone talking about “the next Tesla.” Now March had arrived with a reality check, and Sarah was about to make the mistake that separates the permanently broke from the eventually wealthy.

She was about to sell everything.

I Know Exactly How Sarah Felt

I was 29 when I first discovered my own money brain was my worst enemy. I’d spent two years building what I thought was a diversified portfolio — tech stocks, REITs, even some Bitcoin. Then 2018 happened. I watched $23,000 disappear in six weeks.

The panic was physical. I’d check my brokerage app every morning and feel my chest tighten. My sleep disappeared. I found myself googling “recession signs” at 2 AM, convincing myself I needed to get out before it got worse.

So I sold. Not everything, but close. I locked in a $19,000 loss and moved most of my money to a savings account earning 0.1% annually. I told myself I was being “smart” and “risk-aware.”

What I was actually being was human.

Your Brain Is Wired To Keep You Poor

Here’s what nobody tells you about behavioral finance patterns that keep you poor: your brain evolved to keep you alive in a world of immediate physical threats. It did not evolve to make you wealthy in a world of compound interest and market volatility.

When Sarah saw her portfolio dropping, her amygdala — the ancient part of her brain responsible for fight-or-flight responses — started screaming. It doesn’t understand the difference between a charging mammoth and a temporary market correction. Both register as “DANGER. REACT NOW.”

This is why 97% of people buy high and sell low, despite knowing better intellectually. Your money psychology mistakes average people make aren’t about intelligence. They’re about 200,000 years of programming that worked brilliantly for hunting and gathering, but fails spectacularly at building capital.

Loss aversion hits twice as hard as gain attraction. When you lose $1,000, the pain feels equivalent to the pleasure of gaining $2,000. Your brain treats money losses like physical injuries.

The Pattern Rich People Recognize (And Break)

Back to Sarah in the parking lot. She had her finger hovering over the sell button when her phone buzzed. Text from her older sister Emma — 34, owns three rental properties — who’d seen Sarah’s panicked message from the night before.

“Coffee. Now. Don’t touch anything until we talk.”

Twenty minutes later, Emma was sliding into the booth across from Sarah. “Show me your screen time from this week,” she said.

Sarah reluctantly opened her iPhone settings. Market apps: 4 hours, 37 minutes daily. Financial news: 2 hours, 18 minutes. Investment forums: 1 hour, 43 minutes.

“Eight and a half hours a day,” Emma said. “You’re not investing anymore. You’re gambling and calling it research.”

Emma pulled out her own phone. Her market app screen time: 11 minutes for the entire week.

“Here’s the thing,” Emma continued. “Rich people don’t avoid behavioral biases in personal finance. They build systems that make those biases irrelevant.”

Why Your Brain Sabotages Money Decisions

Think about this: when did you last make a money decision based purely on logic?

If you’re honest, the answer is probably never. Every financial choice you make gets filtered through emotional shortcuts your brain developed when humans lived in caves.

Recency bias makes you think whatever happened last week will keep happening forever. When markets go up, you feel like genius investor. When they drop, you feel like the world is ending. Your brain gives recent events 10x more weight than long-term patterns.

Confirmation bias turns you into your own worst financial advisor. You unconsciously seek information that confirms what you already believe and ignore everything else. Bought GameStop at $200? Suddenly every Reddit post about diamond hands feels like prophecy.

Anchoring bias locks you into the first number you see. You buy a stock at $50, it drops to $35, and your brain refuses to accept the new reality. The $50 becomes your anchor. You hold and hope instead of cutting losses or buying more at the better price.

I learned this the hard way in 2019. I bought shares of a software company at $78 each. When it dropped to $52, I couldn’t bring myself to add more shares because $78 was burned into my brain as the “right” price. Meanwhile, the fundamentals hadn’t changed. The business was growing. I was just anchored to an arbitrary number from six months earlier.

How Rich People Think Differently About Money

Emma wasn’t born wealthy. She was born with something more valuable: a grandfather who understood that behavioral finance patterns that keep you poor can be reversed with the right systems.

“When I was 22,” Emma told Sarah, “I wanted to start investing but knew I couldn’t trust my emotions. So I automated everything.”

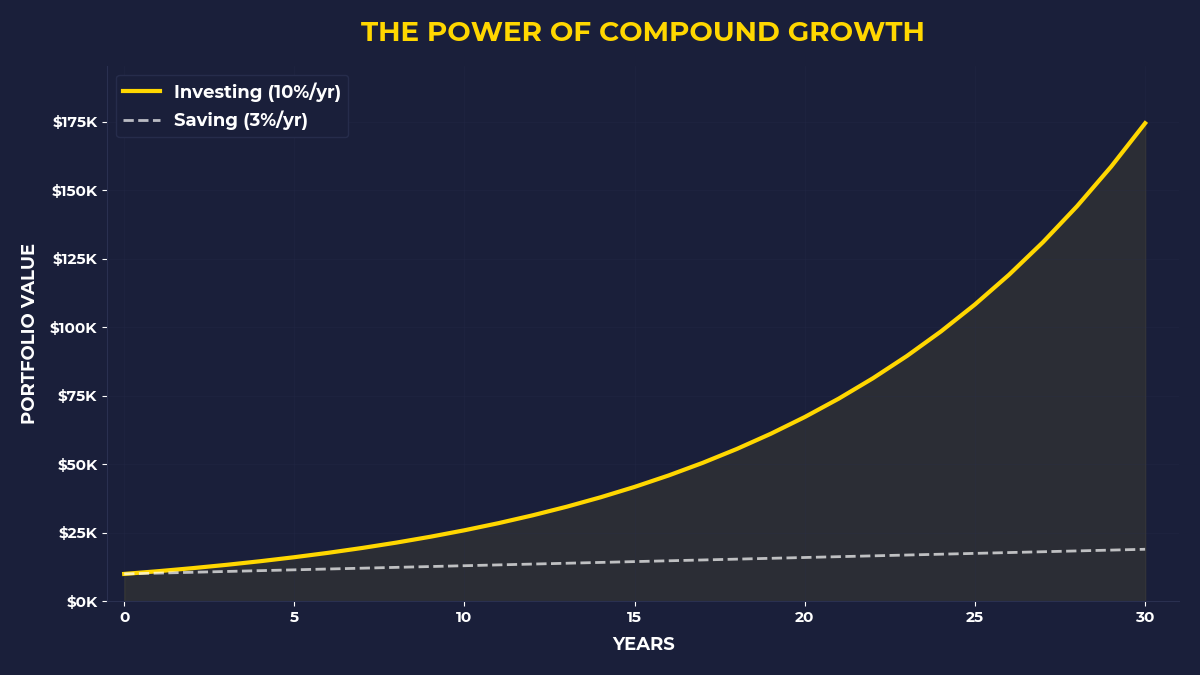

Emma set up automatic transfers that moved $800 from her checking account into index funds every month. No matter what. Market up, market down, recession, boom — the money moved without her permission or input.

“The first year was torture,” she admitted. “I’d see my account balance go down and want to stop the transfers. But I couldn’t. The decision was already made.”

After three years, something shifted. The volatility stopped feeling personal. The account balance became background noise, like checking the weather. She was no longer emotionally attached to daily fluctuations.

By year five, she’d accumulated enough to make her first real estate down payment. Not because she was smarter than everyone else, but because she’d designed a system that made her behavioral biases irrelevant.

The One System That Changes Everything

Sarah left that coffee shop with a plan. Not a complex investing strategy or a detailed financial education curriculum. A simple system designed to work with her psychology, not against it.

She moved her investing apps off her home screen. Deleted the financial news bookmarks. Set up automatic monthly investments that she couldn’t easily modify.

Most importantly, she created what Emma called a “cooling off” rule: before making any investing decision driven by emotion, she had to wait 48 hours and write down three reasons why the decision made logical sense beyond how she was feeling in the moment.

Six months later, Sarah’s portfolio had recovered and grown past her original January peaks. Not because markets only go up, but because she’d stopped interfering with compound growth.

The One Thing To Remember

Your brain will never stop trying to sabotage your wealth. Evolution programmed you to prioritize survival over accumulation, immediate safety over long-term growth. The people who build real capital aren’t the ones with superior willpower or higher IQs. They’re the ones who accept their psychological limitations and build systems that make their biases irrelevant. Rich people don’t fight their money brain — they make it obsolete.

Here’s what you can do today:

- Move $100 into a brokerage account and buy an index fund, even if it means eating ramen this week — especially then

- Delete every market app from your phone’s home screen and turn off all financial news notifications

- Write down the next money decision you want to make, then wait 48 hours before acting on it

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.