Marcus — 29, software engineer in Denver — called me last Tuesday at 11:47 PM. His voice had that hollow quality you get when you’re staring at your laptop screen in the dark, realizing something terrible about your life.

“I just calculated it,” he said. “I’ve been investing for six years. Following all the rules. Dollar-cost averaging into index funds, maxing my 401k, reading every finance blog. My portfolio is up 47% since I started.”

He paused. I could hear him breathing.

“But my rent went up 52% in the same period. My landlord’s making more money off me than I am off my investments. And he’s not even trying.”

I Spent Ten Years Building Someone Else’s Wealth Machine

I know exactly how Marcus felt because I was that guy for most of my twenties.

I had what I thought was a solid investment philosophy. Buy the dip. Stay diversified. Think long-term. I read Bogleheads forums like they were scripture. I could explain the efficient market hypothesis at dinner parties. I felt so smart watching my portfolio creep upward each year.

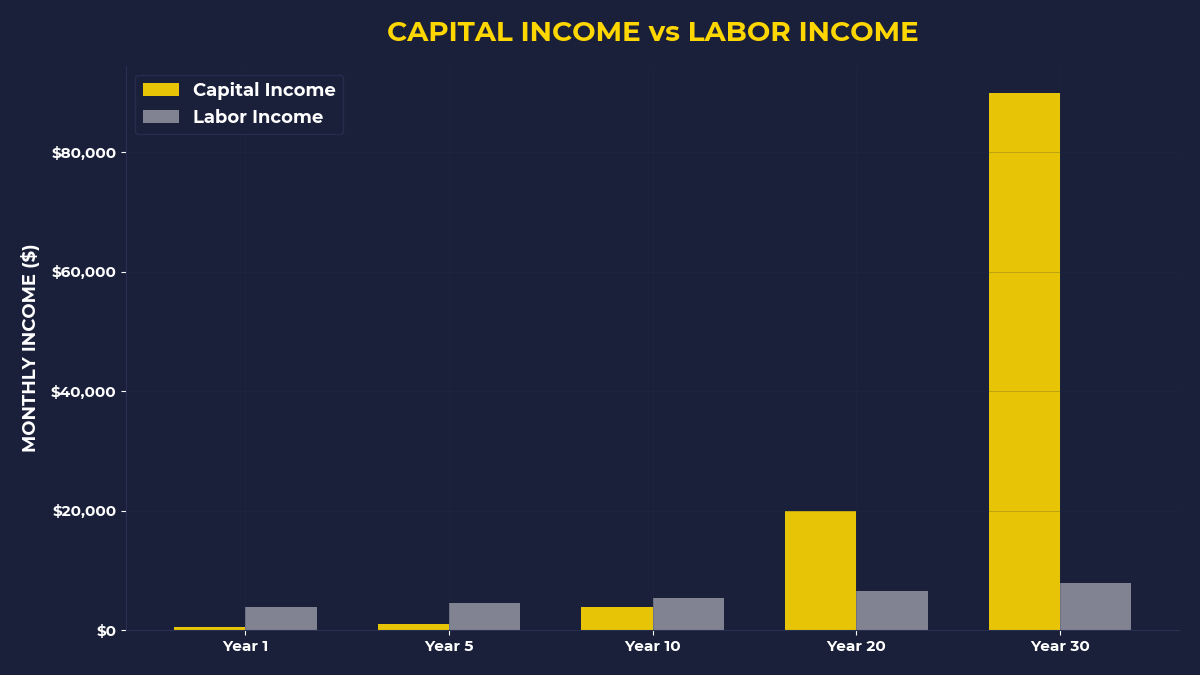

Here’s what I didn’t realize: my entire investment philosophy was designed by people who were already rich.

The advice that dominated every finance blog, every investment book, every retirement calculator — it all assumed I had decades to compound money I didn’t need. It assumed my biggest problem was getting market returns, not getting capital.

But when you’re 26 and paying $1,400 in rent every month, market returns aren’t your problem.

Your problem is that you’re systematically transferring wealth to people who own things while you own nothing but promises about future returns.

The Philosophy That Keeps You On The Wrong Side

Most people’s investment philosophy boils down to this: “I’ll save money from my job and invest it in the stock market for 30 years.”

Sounds reasonable, right?

But think about what that really means. You’re taking money you earned by trading your time and giving it to people who already own income-producing assets. You’re hoping that in three decades, you’ll have enough to stop working.

Meanwhile, every single month, you’re writing checks to people who figured this out already. Your landlord doesn’t wait 30 years to see returns. Your car payment goes to someone who owns the financing company. Your Netflix subscription flows directly to shareholders who bought the equity when it was cheap.

The conventional investment philosophy trains you to be patient while other people collect your impatience tax.

It’s brilliant, actually. Completely backwards for you, but brilliant for them.

What Changed My Mind About Everything

Three years ago, I was grabbing coffee with a friend who owns four rental properties in Austin. Nothing fancy — just decent houses in neighborhoods that were still affordable in 2019.

“I don’t really invest in the stock market anymore,” she told me. “My tenants do that for me.”

I asked her what she meant.

“Look, my renters are mostly young professionals. They make good money. They probably have investment accounts, 401ks, the whole thing. They’re following all the right financial advice.”

She stirred her coffee.

“But every month, they pay me $2,100 in rent. I use $800 of that to cover my mortgage. The other $1,300 is profit. I take that profit and buy more real estate. They’re funding my capital expansion with money they could be using to buy their own capital.”

That conversation broke something in my brain.

She wasn’t smarter than her tenants. She wasn’t working harder. She’d just flipped the script. Instead of saving money to invest later, she’d invested money to save later. Instead of trading time for money and then money for assets, she’d gone straight to the assets part.

Her investment philosophy was simple: buy things that make other people pay you.

The Question That Changes Everything

Want to know if your investment philosophy is working for you or against you?

Ask yourself this: “What did I buy this month that will pay me back?”

Not “What did I invest this month?” — that’s too vague. Not “What did I save?” — savings don’t pay you back, they just sit there losing to inflation.

What did you actually buy that will send you money?

If your answer is “Well, I put $500 into my index fund,” you’re still thinking like someone who trades time for money. You bought a tiny slice of companies that might pay dividends someday and hopefully go up in value over decades.

That’s not wrong. But it’s not capital thinking.

Capital thinking sounds like: “I bought a domain name and built a simple website that generates $200 a month in affiliate revenue.” Or: “I found a duplex where the rent from both units covers the mortgage plus $400.” Or: “I bought shares in a REIT that pays me $50 every quarter.”

The difference isn’t the size of the return. It’s the speed of the feedback loop.

Why Everyone Gets Your Money Before You Do

Here’s what’s really happening with most people’s money:

You earn $5,000. Your landlord gets $1,500. Your car payment takes $400. Insurance companies get $300. Credit card companies take $200. Grocery stores get $600. Utilities get $150. Your phone company gets $80. Netflix gets $15. Spotify gets $10. Your gym gets $50.

You’re left with maybe $1,700.

You save $500 of that. You invest $300. You spend the rest on clothes and going out and trying to feel human after working all week to fund other people’s capital.

Look at that list again. Every single payment except the savings and investing goes to someone who owns something. They’re not trading time for that money — they own assets that generate it automatically.

Your monthly expense sheet is a map of the capital you don’t own.

The Contrarian Move Nobody Talks About

Last month, I met Sarah — 32, marketing manager in Seattle — who’d figured out something most people never learn.

“I stopped maxing my 401k,” she told me. “I know that sounds crazy. But I dropped my contribution from 15% to 6% and used the difference to buy a food truck.”

The food truck makes about $800 a month in profit after expenses. She parks it near a community college three days a week and at office complexes the other two days.

“Everyone told me I was giving up free money by not maxing the 401k match,” she said. “But the food truck pays me $800 a month right now. My 401k might pay me in 30 years.”

Here’s what Sarah understood that most people miss: there’s a difference between building wealth and deferring poverty.

Maxing your 401k is deferring poverty. You’re hoping you’ll have enough money decades from now to stop working. It’s defensive.

Buying cash-flowing assets is building wealth. You’re creating income streams that reduce your dependence on trading time for money. It’s offensive.

The contrarian move is to prioritize immediate cash flow over theoretical future value.

If You’re Tired of Making Other People Rich

This post is for you if you’re making decent money but still feel like you’re falling behind. If you invest regularly but can’t shake the feeling that the game is rigged. If you’re following all the financial advice but your landlord seems to be doing better than you are without trying as hard.

It’s for you if you’ve ever wondered why people who own things seem to have life figured out while people who work for things are always stressed about money.

It’s not for you if you’re already financially independent or if you love your job so much that you never want to stop doing it.

And it’s definitely not for you if you think the stock market is a casino. This isn’t about getting rich quick. It’s about reorienting your entire relationship with money around ownership instead of speculation.

The One Thing To Remember

Your investment philosophy isn’t neutral. It’s either designed to make you wealthy or to make you a wealth transfer mechanism for people who are already rich. The traditional approach — save money, invest in diversified funds, wait 30 years — keeps you on the labor side of the economy while systematically feeding the capital side. The contrarian approach flips this: prioritize buying things that pay you back immediately, even if it means temporarily reducing your long-term investments. Your monthly expenses reveal exactly where your capital should be going.

- Before you pay any non-essential bill this month, ask: “Could I buy a piece of what I’m about to pay for instead of just paying for it?”

- Find one expense over $100/month that goes to a capital owner and research if you could own that type of asset instead

- Set a rule: for every dollar you put in long-term investments, put 50 cents toward something that could pay you back within 12 months

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.