Sarah — 29, marketing coordinator in Portland — sat in her car after her quarterly review, staring at the $7,200 bonus check in her hands. Her boss had praised her campaign that drove $340,000 in new revenue. The smart move was obvious: invest it. The S&P 500 was down 18% from its peak. Everything she’d read said buy the dip.

Instead, she drove straight to Chase and deposited every penny into her savings account.

Six months later, the market had bounced back 24%. Her savings earned $14 in interest. That same $7,200 invested would have been worth $8,928. She’d lost $1,714 by being “safe.”

Sarah isn’t stupid. She has an MBA. She reads financial blogs. She knows the data on long-term returns. Yet when it mattered, her brain hijacked her logic and steered her into the worst possible choice.

I Used to Think I Was Different

I remember sitting in my apartment in 2008, watching my 401k balance drop $3,400 in a single week. The financial crisis was unfolding on every screen. My coworkers were panic-selling everything.

I told myself I was smarter than the crowd. I’d read about behavioral finance. I knew about loss aversion and herd mentality. I was going to be contrarian.

Then I looked at my checking account balance: $847. My rent was $1,200, due in eight days.

I sold half my positions.

Not because of some brilliant analysis. Not because I’d discovered some fundamental flaw in my investment thesis. I sold because my brain was screaming that I needed that money for survival, even though those were long-term retirement funds I wouldn’t touch for 30 years.

That’s when I learned something textbooks never taught me: your money brain doesn’t care about your financial education. When you’re scared, it takes over completely.

Your Stone Age Programming Versus Modern Markets

Here’s what behavioral finance gets wrong. It treats your bad money decisions like character flaws you can fix with willpower and better information.

That’s not how brains work.

Your brain was designed 200,000 years ago for a world where losing resources meant death within days. When the mammoth hunt failed, your ancestors who hoarded every scrap of food survived. The ones who took risks starved.

Fast forward to today. Your boss mentions “restructuring” and your amygdala floods your system with the same chemicals that helped cavemen survive famines. Suddenly, putting money in “risky” stocks feels like throwing meat to wolves while your family starves.

The problem isn’t that you’re weak. The problem is that you’re running advanced financial software on ancient hardware.

Think about Sarah’s bonus check. Her conscious mind knew the market was on sale. But her unconscious mind saw her savings account balance and thought: “This is all we have between us and being homeless.” Every fiber of her being screamed to hoard that money.

The Fear Response That Keeps You Poor

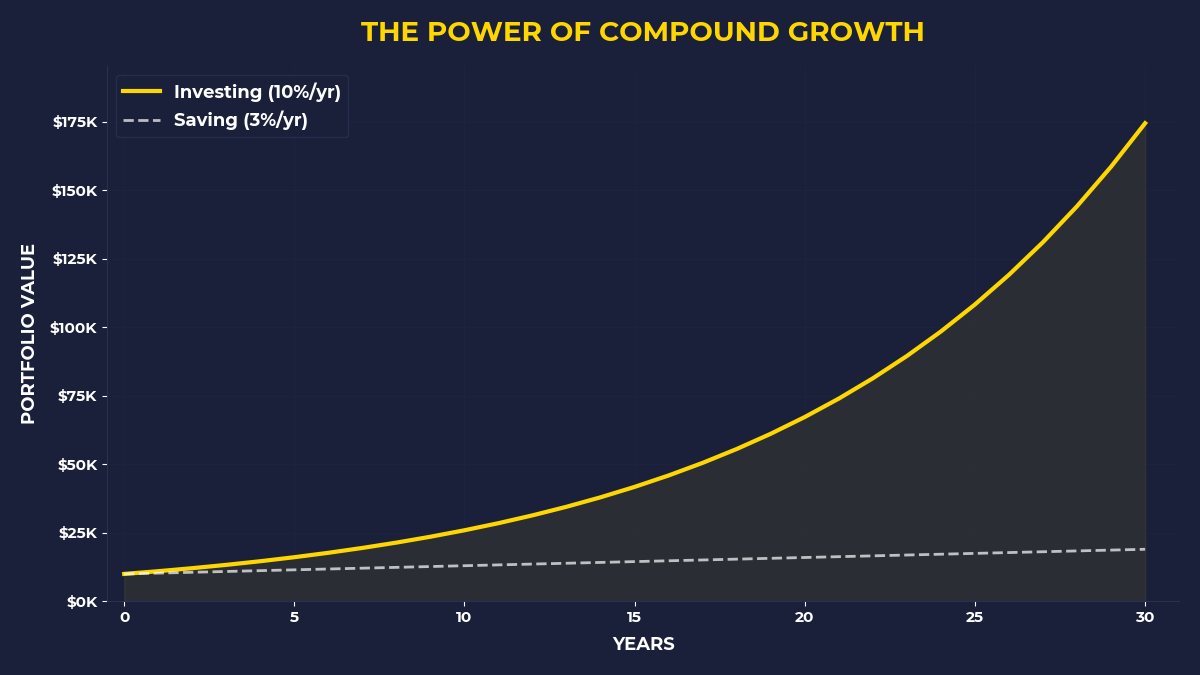

Want to know why 87% of Americans have less than $5,000 invested in the stock market, even though it’s returned 10.5% annually for the past century?

It’s not because they don’t know about compound interest.

It’s because their fear response has been weaponized against them. Every time markets drop 10%, financial media floods them with images of breadlines and homeless camps. Their brain interprets this as: “Investing equals immediate danger.”

Meanwhile, the people getting rich understand something crucial: markets go down precisely when buying opportunities are best. But your brain experiences this backwards. When stocks are expensive and “safe” — like during bubble peaks — you feel confident. When they’re cheap and likely to generate great returns — like during crashes — you feel terrified.

I watched this play out with my friend Mike in 2020. Engineer, $95,000 salary, zero debt. In February, he was excited about finally starting to invest. Had his whole plan mapped out.

Then March happened. Markets dropped 34% in five weeks. Mike didn’t invest a single dollar. “Too risky right now,” he said. “I’ll wait for things to stabilize.”

By the time things felt “stable” again, the S&P 500 was 50% higher than its March lows.

Why Smart People Make The Dumbest Money Choices

Here’s the cruel irony: the smarter you are, the more elaborate the stories your brain creates to justify fear-based decisions.

Sarah didn’t just panic. She rationalized. “The market could drop another 30%,” she told herself. “I should wait for more certainty.” Her MBA gave her enough financial vocabulary to dress up anxiety as analysis.

Smart people are especially vulnerable to what behavioral finance calls “analysis paralysis.” They research endlessly, waiting for the perfect moment, the perfect strategy, the perfect entry point. All while inflation eats their cash and opportunities pass them by.

I see this constantly. A doctor with a $300,000 income will spend three months comparing expense ratios on index funds — a difference of maybe $50 per year — while keeping $40,000 in a savings account earning 0.1%.

Why? Because researching feels productive while actual investing feels dangerous.

The Capital Owners Play a Different Game

People who build serious wealth don’t overcome behavioral finance traps through superior willpower. They design systems that work around their broken programming.

Take automatic investing. When you set up a system that moves $500 from checking to your brokerage account every month, you’re not making a daily decision to “risk” money in the market. The decision was made once, when you felt confident and logical. Your future scared self can’t sabotage it.

Warren Buffett talks about this constantly. He doesn’t try to time markets based on how he feels. He’s programmed himself to buy when others are panicking and hold when others are euphoric.

But here’s the deeper insight: capital owners understand that behavioral finance traps aren’t bugs in the system — they’re features.

Every time regular people panic-sell at market bottoms, they’re transferring wealth to patient buyers. Every time someone keeps their money in 0.1% savings accounts because stocks feel “too risky,” they’re ensuring that actual owners capture all the upside.

The One Decision That Changes Everything

You can’t rewire 200,000 years of evolution. But you can acknowledge that your financial instincts are completely backwards and design around them.

The most important behavioral finance insight isn’t about markets. It’s about timing. Your brain makes the worst money decisions exactly when the stakes are highest.

When you’re stressed about bills, you’ll avoid “risky” investments and keep money in accounts that guarantee you lose to inflation.

When markets crash and opportunities are everywhere, you’ll find a thousand reasons why this time is different.

When everyone around you is getting rich in some obvious bubble, you’ll convince yourself you’re missing out.

The people who build capital understand this and flip the script. They make their most important financial decisions when they’re calm, then automate everything so their panicked future self can’t interfere.

If you’re someone who wants to build wealth but finds yourself paralyzed by financial decisions, here’s your starting point: stop trying to outsmart your brain and start designing around it.

The One Thing to Remember

Your brain is not broken — it’s just running software designed for a world that no longer exists. The same fear response that kept your ancestors alive will keep you poor if you let it drive your financial decisions. Capital owners don’t have better brains; they have better systems that work around their faulty programming.

Set up automatic investing before your next paycheck hits — when you feel optimistic about money, not when you’re stressed about bills

Write down your investment plan when markets are calm, then follow it exactly when they’re chaotic

Never make major financial decisions within 48 hours of reading scary headlines or checking your portfolio during a crash

🎬 Prefer watching? Check out the video version on YouTube: