The Hardest Workers I Know Are Also the Poorest

My neighbor works 70 hours a week. Two jobs, weekend shifts, overtime whenever possible. He’s been doing this for fifteen years. His checking account still hits zero before payday.

Meanwhile, the guy who owns the building where my neighbor works? He showed up twice last month. His net worth grew by more than my neighbor’s annual salary while he was on vacation in Italy.

Here’s what nobody wants to admit: hard work without capital ownership is just expensive labor. You can grind yourself into the ground, optimize every productivity hack, master every skill — and still end up broke at 65 because you fundamentally misunderstand what creates wealth.

The difference isn’t work ethic. It’s not intelligence. It’s not even luck.

The difference is that one person trades hours for dollars, while the other owns systems that generate dollars automatically.

I Used to Believe in the Time-Money Exchange

I spent my twenties convinced that working harder would make me richer. If I could just get promoted, land that next client, bill more hours — then financial freedom would follow. I was optimizing the wrong variable entirely.

The awakening came when I calculated my effective hourly rate as a “successful” consultant. After factoring in unpaid business development, admin work, and the mental energy I spent thinking about client problems at 2 AM, I was making less per hour than someone managing a retail store.

That’s when I realized the brutal truth: time is the one asset you can never get back, and trading it for money is the slowest possible path to wealth.

Look around. Every bill in your mailbox represents someone who figured this out before you did.

Your Monthly Bills Are Invoices From Asset Owners

Open your statement from last month. Really look at it.

Rent or mortgage payment? That’s your landlord or bank collecting returns on their real estate capital. Electric bill? The utility company owns the infrastructure that powers your life. Netflix subscription? They own the platform and content library that entertains you. Car payment? The bank owns the loan, the manufacturer owns the brand.

Even your morning coffee — someone owns the beans, the supply chain, the shop, the equipment, the location lease.

Your paycheck flows to asset owners before it flows to you. And here’s the psychological trap: this feels normal because everyone does it. Your brain categorizes these payments as “necessary expenses” instead of what they really are — transfers of your labor value to people who own things.

The primitive instinct at work here is social conformity. We do what the tribe does. The tribe works for money, then sends that money to asset owners. Questioning this pattern feels dangerous because it means admitting the game is rigged in favor of owners.

What Warren Buffett Learned Selling Golf Balls

When Buffett was twelve, he found lost golf balls near local courses and sold them for fifty cents each. Pure labor — his time and effort converting into immediate cash. Classic time-for-money exchange.

But then he did something different. Instead of just pocketing the money, he used those profits to buy his first stock — three shares of Cities Service Preferred at $38 per share in 1942. He was buying a piece of demand rather than creating it himself.

That shift from “What work should I do?” to “What assets should I buy?” changed everything. By age 30, Buffett’s investment returns were generating more than most people’s salaries. By 40, his assets were working harder than he ever had to.

The compound effect wasn’t just mathematical — it was structural. Each dollar he earned from assets could buy more assets, which generated more dollars, which bought more assets. Meanwhile, his golf ball competitors were still trading hours for quarters.

Capital Is Stored Demand, Not Stored Labor

Think about why famous singers make millions while talented street performers make tips.

Is it because the famous singer works harder? Practices more? Has better vocal technique? Not necessarily. The difference is that the famous singer owns something scarce that millions of people want: their recorded music, their brand, their platform, their fanbase.

That’s capital. Not money sitting in a bank account — stored demand.

When you own capital, you own the right to say yes to opportunities and no to everything else. When you only own your labor, you have to say yes to whatever pays the bills this month.

The wealthy understand this instinctively. According to the Federal Reserve’s 2022 Survey of Consumer Finances, the top 10% of Americans hold 89% of all stocks and mutual fund shares. They’re not just saving money — they’re buying pieces of other people’s demand.

Why Your Brain Sabotages This Transition

Here’s the hardest part: your ancient wiring actively fights against capital thinking.

Loss aversion makes you hoard cash instead of investing it. Recency bias makes you avoid stocks after market drops and chase them after rallies. Social proof makes you copy your broke friends instead of studying wealthy strangers.

Most destructively, your brain equates “working” with “earning.” This made sense when humans lived in small tribes where your daily effort directly determined your daily food. But in a capital-based economy, this instinct keeps you trapped in the labor game while the capital game runs circles around you.

I know this pattern because I lived it. Every time I had extra money, my first instinct was to keep it “safe” in savings or spend it on something that made me feel productive — another course, better equipment, productivity software.

These felt like investments, but they weren’t. They were just expensive ways to become better at trading time for money.

The Question That Changes Everything

What if you flipped the default?

Instead of asking “How can I work more efficiently?” ask “What can I buy that generates returns without my involvement?”

Instead of “How do I increase my hourly rate?” ask “How do I buy exposure to systems that scale beyond my personal hours?”

Instead of “What skills should I develop?” ask “What assets should I accumulate?”

This isn’t about quitting your job tomorrow. It’s about redirecting the capital you’re already generating toward ownership instead of consumption.

When Robert Kiyosaki was living in a friend’s garage after his business failed, he made one decision that changed his trajectory. Every dollar he earned went to buying assets before paying bills. Not after — before. When he couldn’t pay his bills, he took weekend jobs to cover the gap.

This forced him to think like an owner instead of a worker. The uncomfortable pressure of unpaid bills motivated him to find assets that generated cash flow, rather than just working harder to pay those bills directly.

The Leverage Effect Most People Never See

Here’s what the wealthy understand about assets: they multiply effort instead of just adding to it.

If you work twice as hard, you might earn twice as much — but you also work twice as many hours. Linear relationship.

If you own assets that appreciate or generate cash flow, your wealth can grow while you sleep. Your money works weekends. Your capital doesn’t take sick days.

A friend of mine bought a small apartment building in 2018 for $340,000 with 20% down. His tenants’ rent payments cover the mortgage, maintenance, and generate about $800 monthly profit. The building is now worth $485,000. His total return over five years exceeds what he could have earned working extra hours at his day job — and he spends maybe two hours per month managing it.

That’s leverage. His initial $68,000 down payment is now controlling an asset that generates both cash flow and appreciation, operated by systems and other people.

If You’re Still Trading Time for All Your Money, Start Here

You don’t need to quit your job or start a business to begin this transition. You need to start thinking like someone who owns productive assets instead of someone who just works for them.

The simplest version: take 10% of your next paycheck and buy shares in companies that generate products or services other people want. You’re literally buying pieces of demand instead of just creating it with your labor.

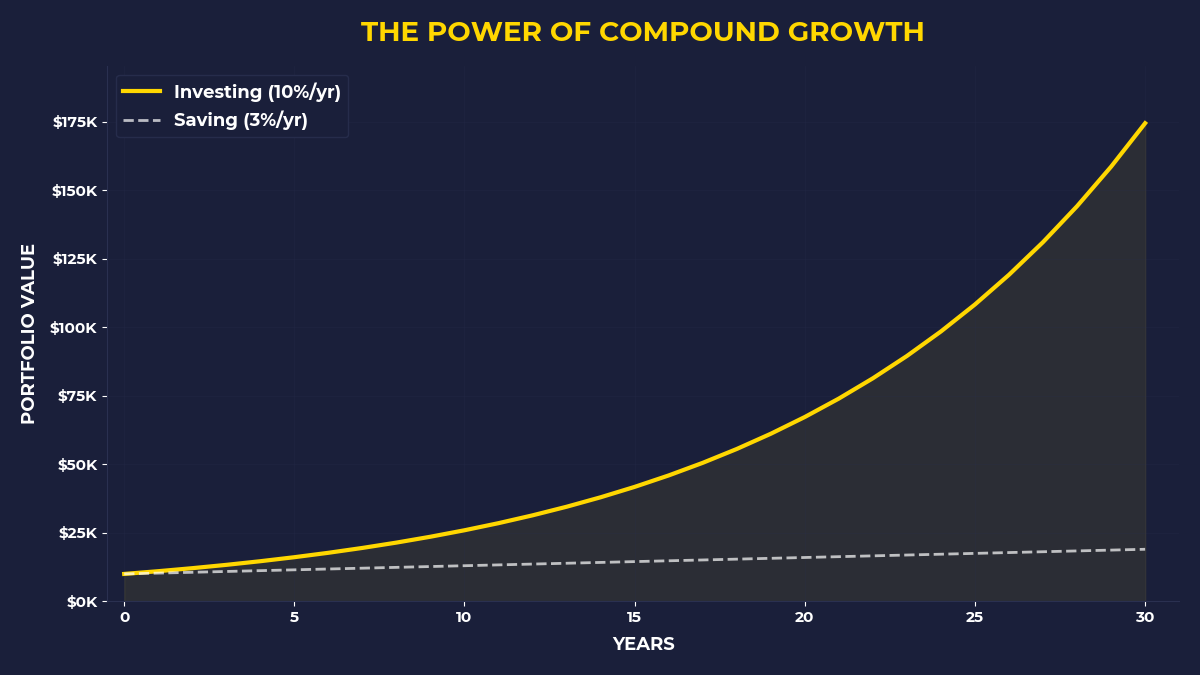

The S&P 500 has generated average annual returns of 10.7% over the past 30 years. That means $100 invested monthly since 1994 would be worth over $200,000 today — assuming reinvested dividends and no additional contributions beyond that initial $100 per month.

But here’s the key: think like an owner, not a speculator. You’re not trying to time markets or pick winners. You’re buying exposure to the productive capacity of businesses that serve demand you can’t serve personally.

What The Primal Investor Takes Away

• Your monthly bills reveal who owns the assets in your life — make sure some of those asset owners are you

• Hard work without asset ownership is just expensive labor that scales linearly with your time

• Ask “What should I buy?” instead of “What should I do?” when you want to increase income

• Start with 10% of income toward assets that generate returns without your active involvement

• Think like an owner: buy pieces of demand rather than just serving demand with your labor

The hardest part isn’t learning how to invest. It’s overriding the ancient wiring that makes trading time for money feel like the only legitimate path to wealth. Your labor has limits. Your assets don’t.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.