Sarah — 29, marketing coordinator in Denver — stood in Target holding a $47 throw pillow. She’d already spent twenty minutes comparing prices, reading reviews on her phone, asking herself if the color would really work with her couch. Meanwhile, her 401k sat at 3% contribution because she “couldn’t afford” to put in more than the company match.

She bought the pillow.

Two hours later, she got a text from her investment app suggesting she increase her monthly contribution by $50. She dismissed it without thinking. Too expensive right now, she told herself. Maybe next month.

Sarah’s brain had just executed a perfect demonstration of behavioral finance in action. She’d spend twenty minutes deliberating over $47 for something that would sit on her couch, but dismissed a $50 wealth-building decision in three seconds. Her brain treated immediate, tangible purchases as worthy of careful consideration, while treating future wealth as an abstract concept not worth the mental energy.

Here’s the thing. Sarah isn’t stupid. She has a business degree. She reads financial blogs. She knows compound interest is important.

But her brain doesn’t care about any of that.

I Made The Same Mistake for Years

I know exactly how Sarah’s brain works because mine worked the same way for most of my twenties. I’d research restaurants for thirty minutes before spending $35 on dinner, but I’d let my savings sit in a 0.01% checking account for two years because “investing seemed complicated.”

I remember one particularly embarrassing moment when I was 27. I spent an entire Saturday comparing prices on a $180 coffee maker, reading seventeen different reviews, watching YouTube unboxing videos. That same week, I had $3,200 sitting in checking that I kept meaning to invest. For six months, I kept meaning to invest it.

The coffee maker research felt productive. Important. The investment decision felt overwhelming and abstract. So I researched coffee makers and let the $3,200 earn nothing.

My brain had categorized these two financial decisions completely differently. The coffee maker was a “purchase decision” — concrete, immediate, requiring careful analysis. The investment was a “someday decision” — vague, future-focused, easy to postpone.

This is behavioral finance in its purest form. The study of how our psychological biases systematically sabotage our money decisions.

Why Your Brain Treats Money Like a Stone Age Threat

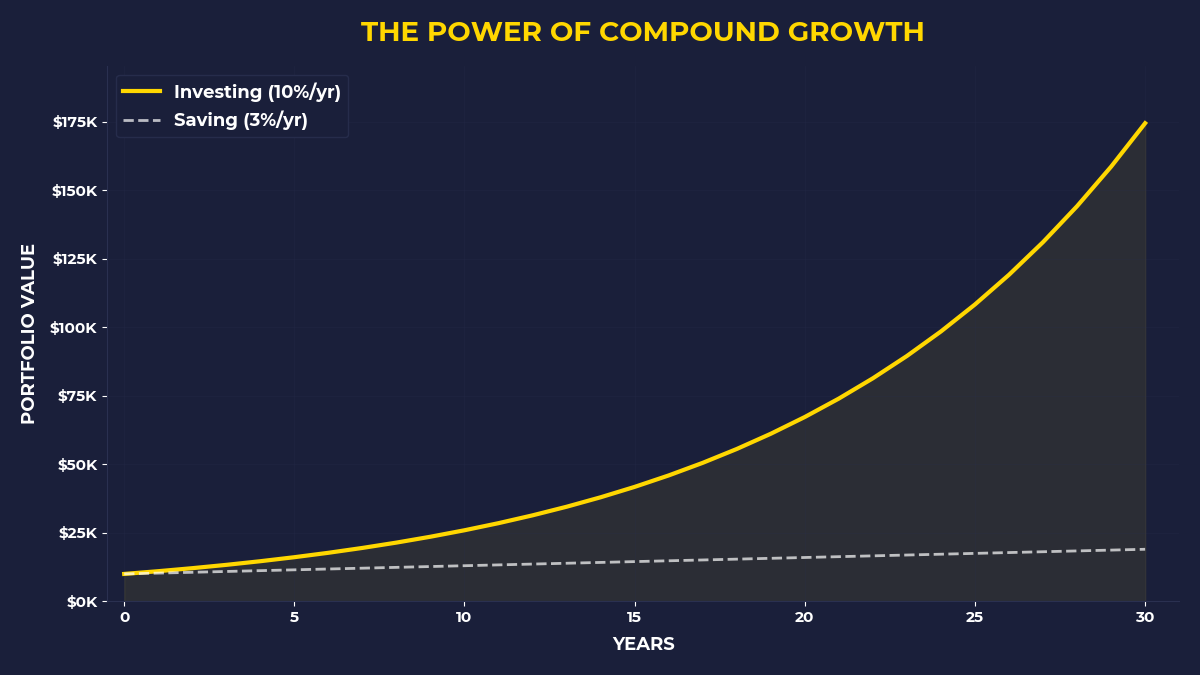

Think about what your brain evolved to do. For 200,000 years, humans lived in small tribes, worried about immediate survival, and never had to think about compound interest or retirement planning. Your ancestors who survived were the ones who could quickly assess immediate threats and opportunities.

Is that rustling bush a predator? Better decide in two seconds or you’re dead.

Should you eat those berries now or save them for later? Eat them now — you might not survive until later.

Your brain still runs on this ancient software. It’s brilliant at handling immediate, concrete decisions with clear consequences. It’s terrible at handling abstract, long-term decisions with delayed payoffs.

This creates predictable patterns that keep most people poor:

Present Bias: Your brain weighs immediate rewards much more heavily than future rewards. The $47 pillow gives you immediate satisfaction. The $50 investment gives you nothing today.

Loss Aversion: Your brain feels the pain of losing money twice as strongly as the pleasure of gaining money. Moving $200 from checking to investment feels like a loss, even though it’s still your money.

Analysis Paralysis: Your brain demands certainty before making important decisions. Since investing involves uncertainty, your brain prefers to make no decision at all.

These aren’t character flaws. They’re programming bugs that affect everyone.

The Billionaire’s Brain Runs the Same Faulty Code

Here’s what makes this fascinating: even billionaires struggle with behavioral finance. Warren Buffett famously keeps 99% of his wealth in Berkshire Hathaway stock — a concentration that would terrify any financial advisor. Charlie Munger admitted he’s “made every mistake in the book” when it comes to behavioral biases.

The difference isn’t that successful investors have better brains. They’ve just built better systems to work around their brain’s limitations.

Buffett doesn’t try to time the market because he knows his brain would trick him into buying high and selling low. Instead, he buys companies he understands and holds them for decades. He’s automated the hardest behavioral finance decisions out of existence.

This is the key insight: you can’t fix your brain, but you can design around it.

The $200 Experiment That Rewires Everything

Want to see behavioral finance in action? Try this experiment next month.

On the first day of the month, before you pay any bills or buy anything, move $200 from checking into a brokerage account and buy an index fund. Don’t think about it. Don’t analyze it. Just do it automatically.

Then go about your month normally. Pay your bills, buy groceries, live your life.

What you’ll discover is fascinating. Your brain will probably panic for about 48 hours. “What if I need that $200? What if there’s an emergency? What if the market crashes tomorrow?”

But by day three, something shifts. Your brain stops thinking about that $200. You’ll naturally adjust your spending to accommodate its absence. You’ll skip the $47 throw pillow. You’ll cook dinner instead of ordering takeout. You’ll find the money somewhere else because your brain now categorizes that $200 as “already spent.”

This is the automation principle. By making the investment decision automatic and immediate, you bypass all the psychological barriers that normally sabotage wealth building.

Why Your Friends Will Think You’re Crazy

Are you someone who’s tired of watching your money disappear into other people’s pockets while your own wealth stays flat? Someone who knows you should be investing but keeps finding reasons to wait another month?

Then you’re going to love what happens when you start prioritizing capital over comfort purchases.

Your friends will think you’re making a mistake. “You can’t afford to invest right now,” they’ll say. “You should pay off all your debt first.” “You should have six months of expenses saved before you start investing.”

This is their behavioral finance talking. Their brains are designed to prioritize immediate security over long-term wealth building. They’re not wrong to worry about emergencies and debt. But they’re applying stone-age thinking to modern wealth building.

Here’s the counterintuitive truth: the best time to start building capital is when you feel like you can’t afford it. That feeling of scarcity is exactly what forces you to make the behavioral changes that actually build wealth.

When you have “extra” money, your brain categorizes investment as optional. When you have to choose between a capital purchase and a comfort purchase, your brain starts learning to choose capital.

The One Thing To Remember

Your brain evolved to keep you alive in the short term, not to make you wealthy in the long term. Every day it runs programs designed to prioritize immediate comfort over future capital. This isn’t a character flaw — it’s human nature. But you can design simple systems that work with your psychology instead of against it. The people who build wealth aren’t the ones with perfect discipline. They’re the ones who automate the hardest decisions and then let their imperfect brains adapt.

Set up automatic investment transfers on the same day you get paid, before you have time to think about it

Track your “capital purchases” (investments) separately from your “comfort purchases” (everything else) for one month

When you want to buy something over $50, wait 24 hours and ask: “Would I rather own this thing or own a piece of something that pays me back?”

🎬 Prefer watching? Check out the video version on YouTube: