Everyone’s asking the wrong question about artificial intelligence. They want to know which jobs AI will destroy. Which careers will survive. How to “AI-proof” their income.

Here’s what they’re missing: AI doesn’t create jobs or destroy them.

AI creates capital.

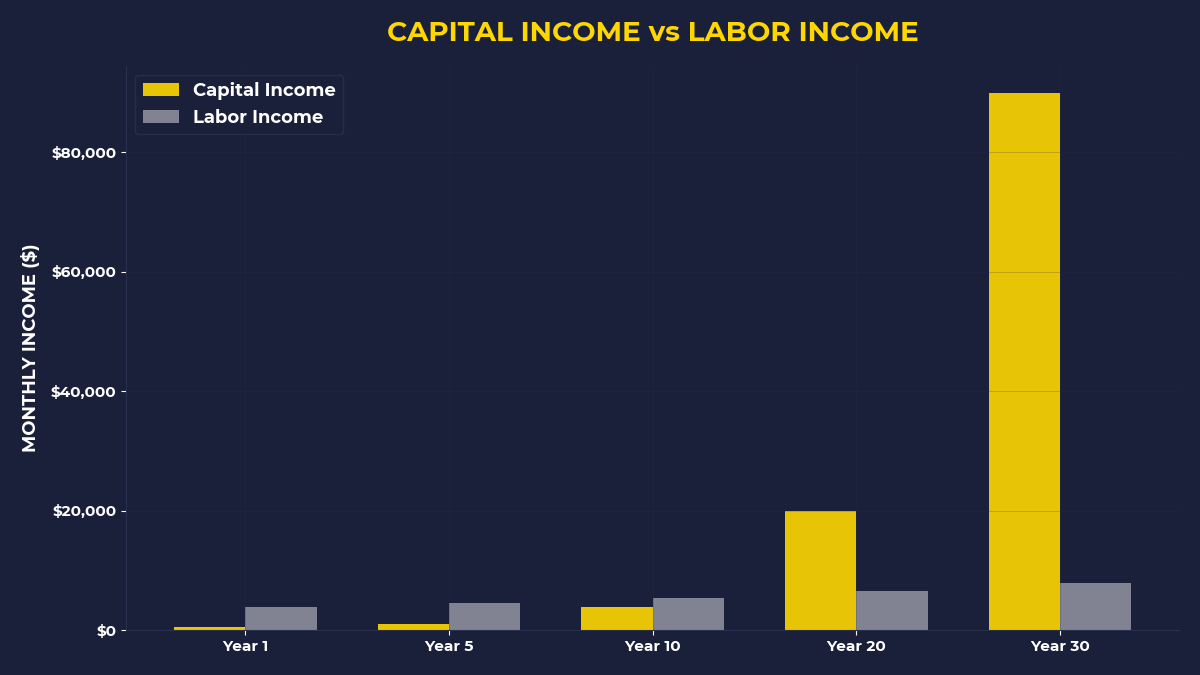

The difference matters more than you think. Jobs pay you for your time. Capital pays you for owning something that generates demand. When ChatGPT writes code in 30 seconds that used to take a programmer 3 hours, that’s not job displacement—that’s capital formation. The question isn’t whether your job is safe. The question is whether you own a piece of the machine doing the work.

I used to think AI was primarily a productivity tool. Something that would make workers more efficient, like Excel did for accountants or email did for communication. I was looking at it through the lens of labor enhancement.

Then I lost money.

When I Bet on the Wrong Side of Intelligence

In early 2023, I bought shares in a company that provided human content moderation services. Smart people, good processes, established client base. The logic seemed sound: as social media grew, someone had to review all that content.

Three months later, their largest client replaced 70% of their human moderators with AI systems.

The stock dropped 43% in two weeks.

Sitting there, watching my position crater, I realized I’d made the classic mistake. I was thinking about AI as a tool that helps humans work better. But AI isn’t a better hammer. It’s a replacement factory that produces the output directly.

The primitive instinct at work here is **pattern matching**—we tend to understand new technologies through the lens of old ones. We called early cars “horseless carriages” because we couldn’t conceive of transportation that didn’t involve horses. Same trap with AI. We’re calling it “artificial intelligence” when we should be calling it “synthetic labor.”

Look at the numbers. Between 1990 and 2020, U.S. manufacturing output increased by 85% while manufacturing employment fell by 35%. The machines didn’t just help workers—they replaced them. But here’s the key insight: the owners of those machines captured all the productivity gains.

Why This Time Actually Is Different

What makes AI unique isn’t its intelligence—it’s its **generalizability**. Previous automation targeted specific tasks. Assembly line robots replaced assembly line workers. Software replaced bookkeepers. Each wave of automation stayed in its lane.

AI jumps lanes.

A single large language model can write marketing copy, debug code, analyze legal contracts, and tutor students in calculus. One system replaces multiple categories of cognitive work. This isn’t task automation—it’s capability replacement.

The economic implications are staggering. When one AI system can perform the cognitive tasks of 50 different roles, the capital efficiency becomes astronomical. Microsoft spent $13 billion on OpenAI and gained access to technology that can replace hundreds of thousands of dollars in annual salaries across multiple functions.

Think about that math. $13 billion divided by even 100,000 replaced positions equals $130,000 per position eliminated. And that’s a one-time cost versus recurring salaries.

The Capital Concentration Effect

Here’s where most people get the story backwards. They focus on job displacement instead of wealth concentration.

When AI replaces human labor, where does the economic value go?

It flows to whoever owns the AI systems. Not the people who built them—the people who own them. The engineers at OpenAI get salaries. The shareholders of Microsoft get the productivity gains, forever.

This is why NVIDIA’s market cap increased by over $1.8 trillion between January 2023 and December 2023. Investors understood that selling shovels during a gold rush means owning the infrastructure of wealth creation. Every company racing to implement AI needs NVIDIA’s chips.

But the real wealth transfer is more subtle. When a company replaces 100 customer service representatives with an AI system, those salary costs don’t vanish—they convert into profit margins. The $4 million in annual salaries becomes $3.8 million in additional earnings for shareholders (after paying for the AI system).

The Demand Storage Insight

Remember: capital is stored demand, not money sitting in a bank account. When customers want customer service, they’re expressing demand. That demand used to require human labor to fulfill. Now AI can fulfill the same demand with less input cost.

The demand didn’t disappear. It just requires less human energy to satisfy.

This is the same principle Warren Buffett understood when he bought See’s Candies in 1972. People’s demand for premium chocolate didn’t change. But owning the system that fulfills that demand—the brand, the recipes, the distribution—meant capturing the economic value without doing the daily work.

AI accelerates this dynamic across every industry simultaneously.

A friend of mine runs a small marketing agency. Fifteen employees, good reputation, steady growth. Last year, he started using AI tools for content creation and data analysis. His output per employee increased by roughly 40%. Instead of hiring more people, he raised prices and kept the extra margin.

His clients get better results. His employees keep their jobs. He captures the productivity gain.

That’s the pattern playing out across the economy. AI doesn’t eliminate demand—it concentrates the economic benefit in fewer hands.

Why the Contrarian Play Isn’t What You Think

The obvious contrarian move seems like betting against AI companies or buying “AI-proof” assets. Human services, local businesses, anything that requires physical presence.

That’s exactly backward.

The real contrarian insight is this: while everyone worries about their jobs, smart money buys ownership in the systems replacing those jobs.

When 70% of people fear AI will eliminate their careers, that creates two opportunities. First, AI-enabled businesses trade at discounts because of perceived “disruption risk.” Second, the companies building AI infrastructure get undervalued because investors focus on short-term implementation costs instead of long-term margin expansion.

Between 2018 and 2021, many investors avoided cloud computing stocks because they were “overvalued.” Amazon Web Services grew revenue from $25.7 billion to $62.2 billion during that period. The fear was wrong. The structural shift was real.

The Ownership Question Nobody’s Asking

Here’s the question that separates future capital owners from future labor renters: What AI-enabled systems can I own pieces of, instead of competing against?

This isn’t about picking individual AI stocks. It’s about understanding that AI amplifies the return to ownership while reducing the return to labor.

If you own shares in companies that successfully implement AI, you benefit from every efficiency gain. If you only sell your labor to those companies, you compete with increasingly capable systems.

The wealth transfer isn’t coming from AI replacing human workers. It’s coming from AI multiplying the productivity of capital while making human labor less necessary.

Look at what happened to Blockbuster versus Netflix between 2007 and 2010. Blockbuster had more employees, more locations, more customer touchpoints. Netflix had a better system for fulfilling the same underlying demand—home entertainment. The demand didn’t disappear when Blockbuster died. It just flowed to whoever owned the superior delivery mechanism.

What The Primal Investor Takes Away

• **AI economics is about capital formation, not job displacement**—when systems replace workers, the economic value flows to system owners, not system users

• **Productivity gains compound for owners but not for workers**—employees might keep their jobs but owners capture the efficiency improvements forever

• **The contrarian play is buying ownership while others fear replacement**—widespread job anxiety creates investment opportunities in AI-enabled businesses

• **Focus on companies implementing AI, not just building it**—the real wealth creation happens when AI reduces costs and increases margins across existing businesses

• **Ask what you can own, not what you can do**—AI amplifies the return to ownership while commoditizing the return to labor

The primitive brain sees AI as a threat to employment. The investor’s brain sees AI as a multiplier of capital efficiency. While everyone else worries about their paycheck, you can position yourself to own the systems generating the paychecks.

🎬 Prefer watching? Check out the video version on YouTube:

")