Your investment philosophy sounds exactly like your performance review. Work hard. Stay disciplined. Focus on what you can control. Save consistently. Diversify responsibly. Think long-term.

Here’s what nobody tells you: that’s employee thinking dressed up as investor wisdom.

I spent my twenties following this script religiously. Dollar-cost averaging into index funds. Reading about asset allocation. Rebalancing quarterly like some kind of financial monk. The whole time, my landlord was collecting rent checks that paid his mortgage, built his equity, and funded his next property purchase. I was optimizing my 401k contributions while he was optimizing his capital structure.

The difference between workers and owners isn’t their investment accounts. It’s their entire framework for thinking about money. Workers think about earnings. Owners think about demand.

What Is Investment Philosophy, Really?

Strip away the jargon and your investment philosophy is just your answer to one question: where should money go to grow?

Most people answer this question the way they’ve been trained to think about work. Put in effort. Get proportional results. Control what you can. Accept what you cannot.

This is why the typical investment philosophy for wealth building sounds like career advice. It’s all about your behavior, your discipline, your consistency. As if the primary variable in wealth creation is how hard you try.

Look at any investment forum. The conversations are obsessed with personal optimization. Which broker has the lowest fees? How often should you rebalance? What’s the optimal savings rate? Should you invest in taxable accounts or max out your IRA first?

These are worker questions. They assume your job is to feed money into the system and hope the system rewards your consistency.

The Capital Owner’s Framework

Owners think differently about where money should go.

When Warren Buffett was 11 years old, he spent $38 on three shares of Cities Service Preferred. That’s about $400 in today’s money. He didn’t buy it because someone told him to diversify or because he wanted to dollar-cost average into the market.

He bought it because he understood something most adults never figure out: companies exist to serve demand, and when you own part of a company, you own part of that demand.

This is the fundamental difference between capital owner mindset versus labor mindset. Workers ask “What should I do with my money?” Owners ask “What demand should I own?”

When you frame it this way, the entire investment industry starts to look strange. Why would you diversify away from the strongest demand? Why would you rebalance out of what’s working into what isn’t? Why would you dollar-cost average into mediocrity when you could concentrate on excellence?

The Employee Investment Philosophy Trap

The standard investment philosophy makes perfect sense if you think like an employee. Employees are taught to minimize risk, follow systems, and trust the process. These are good instincts for keeping a job. They’re terrible instincts for building capital.

Consider the advice to “never put all your eggs in one basket.” This sounds reasonable until you realize that every wealthy person you know has most of their net worth concentrated in one thing: their business, their real estate portfolio, their stock options, their professional practice.

Jeff Bezos didn’t diversify away from Amazon stock. Bill Gates didn’t rebalance out of Microsoft. Your successful contractor friend didn’t dollar-cost average into random real estate markets.

They concentrated on what they understood, what they could influence, and what had the strongest demand characteristics. The worker philosophy would have kept them poor.

Why Do Smart People Follow Employee Investment Strategies?

Fear. Specifically, loss aversion — the primitive instinct that makes a potential loss feel twice as powerful as a potential gain.

This made sense when we were hunter-gatherers. Losing your food store meant death. Taking unnecessary risks with resources was genuinely dangerous.

But in a modern economy, the biggest risk isn’t losing what you have. It’s never accumulating enough to matter. And the employee investment philosophy all but guarantees you’ll never accumulate enough to matter.

I remember sitting in a financial advisor’s office in 2018, listening to him explain why I should spread my money across 12 different asset classes. “You don’t want to put all your eggs in one basket,” he said. Meanwhile, his own wealth came from owning equity in his practice — literally all his eggs in one basket.

The cognitive dissonance was stunning. He was selling me diversification while building his own wealth through concentration.

The Real Contrarian Investment Philosophy

Here’s what contrarian investing actually means: doing the opposite of what employees are trained to do.

Employees are trained to be replaceable. Investors should be irreplaceable. Employees are trained to follow systems. Investors should own systems. Employees are trained to minimize downside. Investors should maximize upside.

The most contrarian thing you can do is concentrate your capital in what you understand and what has durable demand characteristics. This feels dangerous because you’ve been trained to think like someone whose job depends on not making mistakes.

But building wealth isn’t about avoiding mistakes. It’s about making asymmetric bets where the upside far exceeds the downside.

Amazon stock dropped 94% between 1999 and 2001. If you had owned it and held through that crash, you’d have made 127 times your money by 2021. The diversified investor who spread their risk across the entire market would have made about 3 times their money over the same period.

What Demand Actually Looks Like

Demand isn’t abstract. It’s people willing to pay money for something they need or want, again and again.

Your monthly bills are a perfect map of durable demand. Internet service. Phone service. Groceries. Utilities. Rent or mortgage payments. Insurance. These are businesses that collect money from you every month whether you feel like paying or not.

The companies that provide these services don’t need to convince you to buy every month. You’re already trapped in their system. That’s what strong demand characteristics look like.

When you own equity in these kinds of businesses, you’re not hoping the market will go up. You’re collecting a piece of the cash flow that your neighbors generate by living their lives.

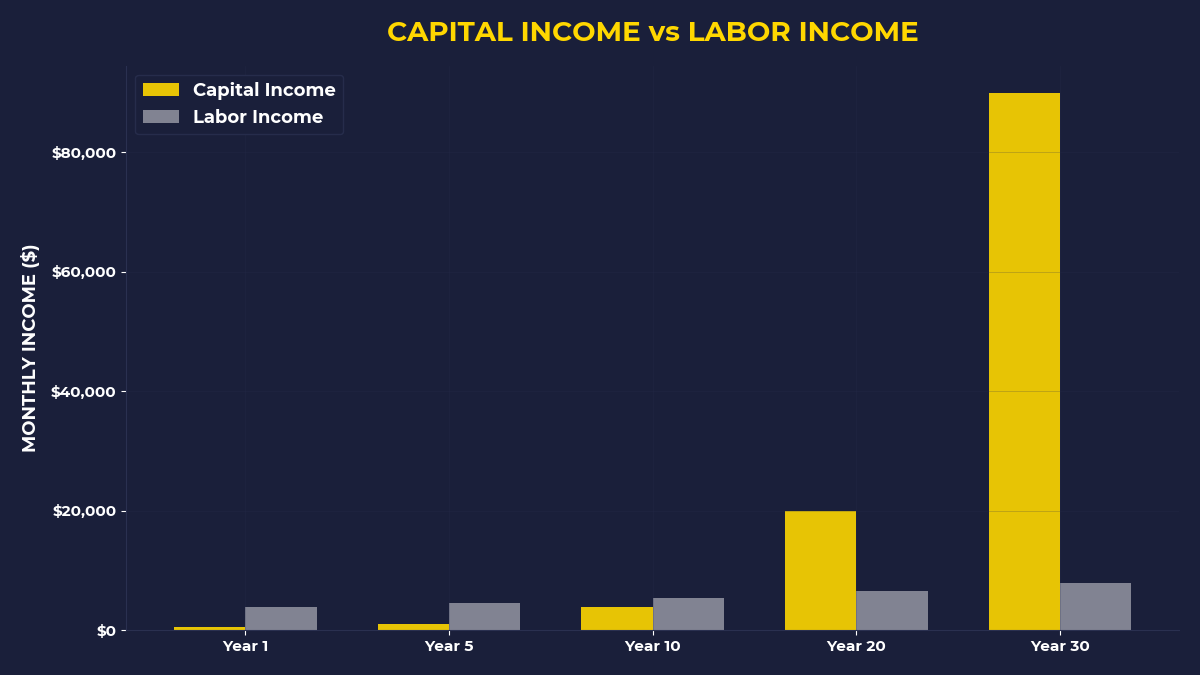

This is why capital compounds while labor just adds up. Labor gets paid once for each hour worked. Capital gets paid continuously for demand served.

Building Your Owner’s Investment Philosophy

Start by asking different questions.

Instead of “How should I diversify?” ask “What demand do I want to own?” Instead of “What’s my target asset allocation?” ask “What systems generate the most reliable cash flow?” Instead of “How do I minimize risk?” ask “How do I maximize my exposure to what’s working?”

The goal isn’t to build a portfolio. It’s to build an ownership stake in the systems that generate demand.

This might mean owning stock in companies that provide essential services. It might mean buying rental property in areas where people have to live. It might mean starting a business that solves a recurring problem.

The specific vehicle matters less than the framework: you’re buying pieces of demand-generating systems, not hoping that financial markets reward your patience.

What The Primal Investor Takes Away

Your current investment philosophy probably sounds like employee training because it is — replace it with an owner’s mindset that focuses on buying demand, not optimizing behavior.

Stop diversifying away from strength — concentrate your capital in what you understand and what has durable demand characteristics instead of spreading risk across mediocrity.

Ask “What demand should I own?” instead of “What should I do with my money?” — this single question shift moves you from worker thinking to owner thinking.

Your monthly bills are a perfect map of strong demand — consider owning equity in the systems that generate these recurring cash flows rather than just paying them.

Accept that building real wealth requires concentration risk — the employee philosophy of avoiding all downside also eliminates most upside.

Remember that capital compounds continuously while labor adds up one hour at a time — your investment philosophy should reflect this fundamental difference.

The worker philosophy keeps you safe and poor. The owner philosophy feels dangerous but builds actual wealth. Choose accordingly.

🎬 Prefer watching? Check out the video version on YouTube:

")