The Morning Sarah’s Bank Account Told Her the Truth

Sarah Martinez — 31, marketing coordinator in Denver — opened her banking app on a Tuesday morning and felt that familiar punch to the stomach. Her $3,200 paycheck had hit on Friday. By Tuesday morning: $127 left.

She pulled up her transactions. Rent: $1,400. Car payment: $480. Student loans: $340. Electric bill: $89. Phone: $95. Insurance: $180. Groceries: $280. Gas: $160. Netflix, Spotify, gym membership: $58. Credit card minimum payment: $190.

Every single dollar had somewhere to go before she even saw it.

Sarah stared at the screen and realized something that made her feel sick. She worked 45 hours a week, but she wasn’t working for herself. She was working for her landlord, Toyota Financial, Sallie Mae, Xcel Energy, Verizon, State Farm, King Soopers, Shell, and Capital One.

Her entire paycheck was just a conduit. It flowed from her employer to a dozen other entities who owned things she needed.

I Used to Send My Money Away Too

I know exactly how Sarah felt because I lived the same cycle for years.

When I was 28, I made $52,000 a year and felt like I was drowning. I’d get my paycheck on Friday and feel rich for about six hours. Then Saturday morning I’d sit down with my laptop and systematically send my money to everyone else.

Rent check: $950. Car payment: $315. Insurance: $140. Utilities: $160. Student loans: $280. Credit cards: $200 minimum payment because I’d charged groceries and gas the week before when I ran out of money.

After paying everyone else, I’d have maybe $300 left for food, gas, and anything unexpected. If my car needed repairs or I got sick, I’d charge it and increase next month’s minimum payments.

Here’s the thing I didn’t understand then: I wasn’t just paying bills. I was paying rent to other people’s capital.

Every payment was a dividend check to someone who owned something I needed to survive.

The Invoice System That Keeps You Poor

Think about your last paycheck. Where did it actually go?

Your rent or mortgage payment went to someone who owns real estate. Your car payment went to someone who owns financing capital. Your student loan payment went to someone who owns educational debt. Your insurance payments went to someone who owns risk management capital. Your utility bills went to someone who owns energy infrastructure. Your grocery bill went to someone who owns food distribution systems.

Even your morning coffee — $4.50 at Starbucks — flows to shareholders of a company that owns thousands of locations and a global supply chain.

You’re not just living paycheck to paycheck. You’re operating as a cash flow generator for capital owners.

The brutal truth: most people spend their entire lives sending their paychecks to people who own assets, while never building assets themselves.

Why This System Is Designed to Keep You Paying

Sarah’s story isn’t unique. According to the Federal Reserve, 40% of Americans can’t cover a $400 emergency without borrowing money or selling something. But here’s what that statistic really means: 40% of Americans live in a system where 100% of their income is spoken for before they receive it.

They have no buffer between earning and spending because every dollar has an owner waiting for it.

This isn’t an accident. Consumer credit, monthly payment plans, and subscription services all exist to capture your future income. When you lease a car instead of saving up to buy one, you guarantee that $400 a month flows from your paycheck to Toyota Financial for the next 36 months.

When you carry a credit card balance, you guarantee that 18% of whatever you charged flows to the bank every year until you pay it off.

The system is designed to make you a reliable income stream for capital owners.

The $50 Experiment That Changed Everything

Two years ago, I had coffee with Robert Kiyosaki’s book Rich Dad Poor Dad fresh in my mind. There’s a story in there that most people skip over. Kiyosaki talks about how his mentor taught him to pay himself first — even when he was broke and living in a friend’s garage.

The mentor’s rule was simple: before you pay any bill, put money aside for assets. Even if it means scrambling to cover rent. Especially then.

I decided to test this with $50 from my next paycheck.

Instead of paying all my bills first and investing whatever was left over (which was usually nothing), I transferred $50 to my brokerage account the moment my paycheck hit. Before rent. Before car payment. Before anything.

Then I had to figure out how to cover my bills with $50 less than usual.

Wild thing: I managed. I ate out one less time that week. I found a gas station that was 8 cents cheaper per gallon. I canceled a subscription I’d forgotten about. I worked two extra hours of freelance writing on the weekend.

But here’s what really changed: for the first time in my adult life, I paid myself before I paid everyone else.

I owned something that would pay me back instead of just sending my money away.

Capital Owners vs. Everyone Else

There are two types of people in the economy: those who own capital and those who pay rent to capital owners.

Capital isn’t just money sitting in a bank account. Capital is anything that generates ongoing demand. Real estate that people need to live in. Companies that provide essential services. Infrastructure that everyone depends on. Brands that people choose consistently.

When you own shares of Apple stock, millions of people around the world buy iPhones and pay for iCloud subscriptions. A tiny fraction of those payments flows to you as dividends and stock price appreciation.

When you don’t own capital, you’re on the other side of that transaction. You’re the one sending money to capital owners every month.

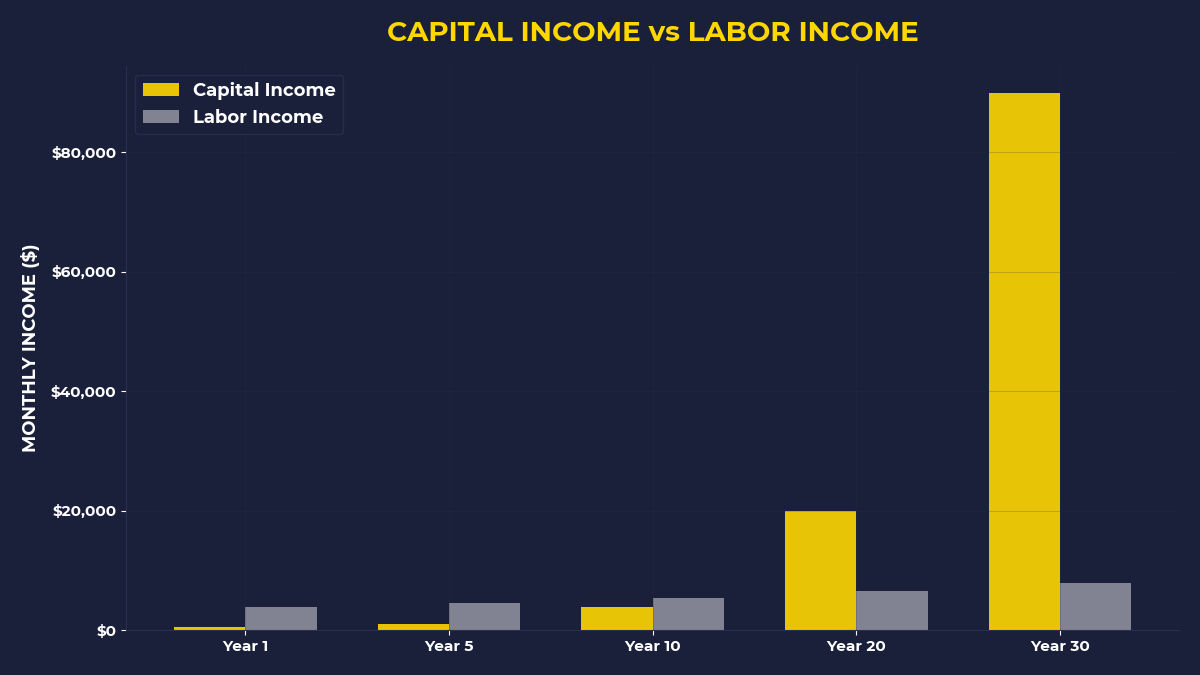

The goal of contrarian investing isn’t to pick stocks that others hate. It’s to gradually switch sides — from being someone who pays capital owners to being someone who receives payments from capital.

The One System That Actually Works

Here’s the framework that changed everything for me:

Before you pay any bill this month — rent, car payment, student loans, credit cards, anything — move money into assets first. Start with whatever amount makes you slightly uncomfortable. Maybe $50. Maybe $200. Maybe $20.

The amount doesn’t matter. What matters is the order.

You pay yourself first by buying ownership in things other people need. Then you figure out how to cover your bills with what’s left.

This forces you to get creative about expenses while building ownership. Instead of automatically sending 100% of your paycheck to other people’s assets, you keep a piece for yourself first.

Over time, the assets you own start generating their own cash flow. Dividend payments. Capital appreciation. Eventually, that income covers some of your bills, freeing up more of your paycheck to buy more assets.

That’s when compound interest becomes your employee instead of your enemy.

If You’re Tired of Working for Everyone Else’s Dreams

This approach isn’t for everyone. If you’re comfortable being a cash flow generator for capital owners for the next 40 years, keep doing what you’re doing.

But if you’re someone who’s tired of watching your entire paycheck disappear before you can use it to build something for yourself, this is how you start switching sides.

If you’re someone who wants to own part of the system instead of just feeding it, this is how you begin.

If you’re someone who’s ready to pay yourself before you pay everyone else, this is your framework.

The One Thing to Remember

Your paycheck doesn’t belong to your bills. It belongs to you first, then to your bills. Every time you pay everyone else before you pay yourself, you’re training yourself to be a permanent income source for capital owners. The moment you flip this order — assets first, bills second — you start the slow process of joining them instead of just feeding them. It’s not about the amount you save. It’s about who gets paid first.

- Before you pay any bill this month, transfer $50 (or whatever makes you uncomfortable) to buy index funds or individual stocks

- Force yourself to cover your regular expenses with the remaining money — get creative, find cuts, work extra hours

- Repeat this every single paycheck, increasing the amount as you get better at living on less

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.